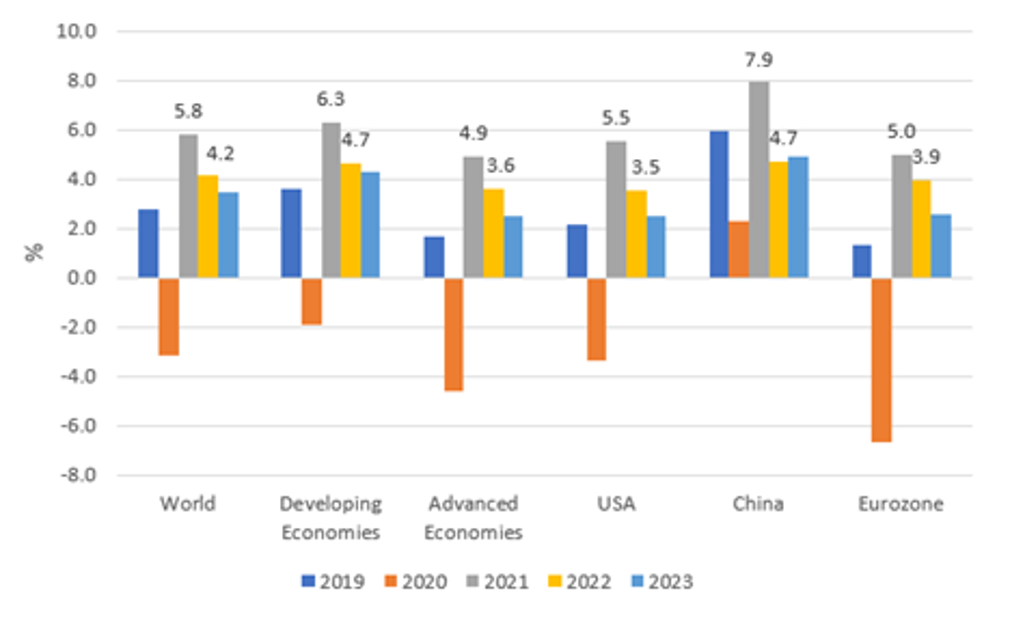

Global real GDP growth is estimated to have reached 5.8% in 2021. In the baseline scenario, global real GDP is expected to increase by 4.2% in 2022 (with a range of 3.2-4.2%) and by 3.4% in 2023 (with a range of 2.2-4.6%). The 2022 global growth forecast represents a 0.6 percentage point downgrade from forecasts in Q4 2021. The downgrade is driven by the emergence of the new highly infectious Omicron COVID-19 variant, the greater expected persistence of current supply constraints, lower than expected fiscal stimulus in the US and worsening conditions in the real estate sector in China.

The global economy remains constrained by the ongoing negative effects of the pandemic, major supply bottlenecks and high commodity and energy prices. Growing problems in China’s real estate and consumer sectors and rising geopolitical uncertainty in Europe surrounding the Russia-Ukraine conflict are also raising downside risks, in addition to the pandemic and inflation uncertainty.

Real GDP Growth Baseline Forecasts: 2019-2023

Source: Euromonitor International Macro Model, National Statistics

Note: (1) Regional real GDP growth using PPP weights; (2) figures for 2021 onwards are forecasts; forecasts updated 18 January 2022

The latest COVID-19 wave has had a much larger number of infections, given the reluctance of countries to impose stricter lockdowns and the high transmission rate of the Omicron variant. However, increases in hospitalisations and death rates have so far been moderate, and considered manageable with the temporary tightening of social distancing restrictions in December and January. The Omicron variant is much more contagious than previous variants, but on average it causes significantly milder symptoms. This may reflect both features of the variant and the high proportion of people who are facing the current COVID-19 wave vaccinated, or with previous recent infection, providing much higher population immunity rates. While the existing vaccines are less effective in preventing infection by new variants, the evidence so far is that they continue to provide robust protection against severe illness.

The main concern with the Omicron wave of infection is that despite its lower severity, its high transmission rate can still lead to overwhelmed healthcare systems. The high transmission rate has also caused staff shortages in affected countries as workers are infected, although the risks of disruption to economic activity have been alleviated by the relaxation of previous quarantine policies for infected workers.

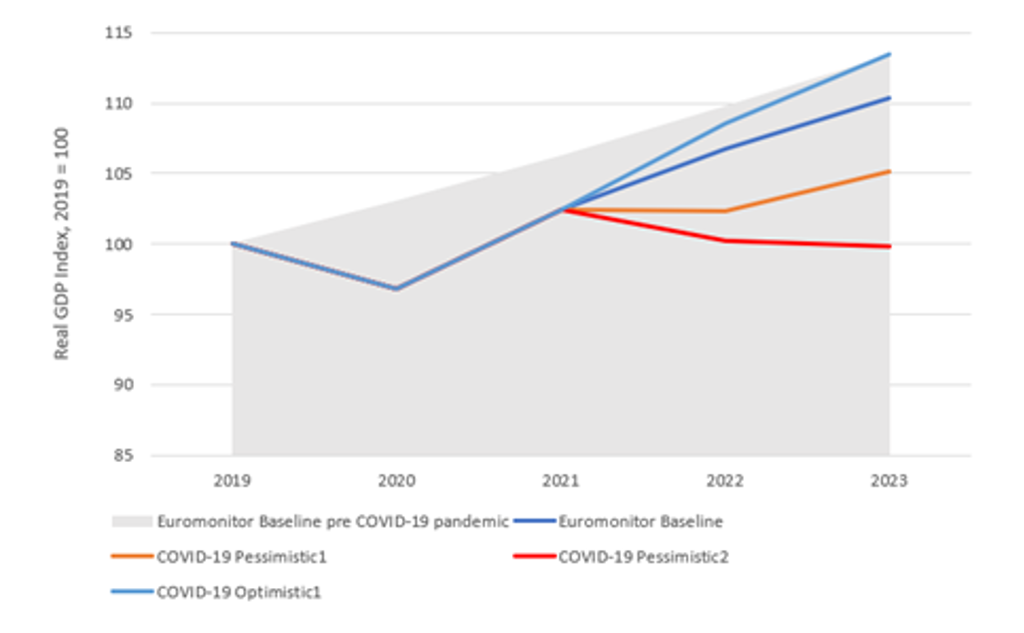

Global Real GDP Index, Baseline and Alternative Scenarios: 2019-2023

Source: Euromonitor International Macro Model, National Statistics

Note: (1) Regional real GDP growth using PPP weights; (2) figures for 2021 onwards are forecasts; forecasts updated 18 January 2022

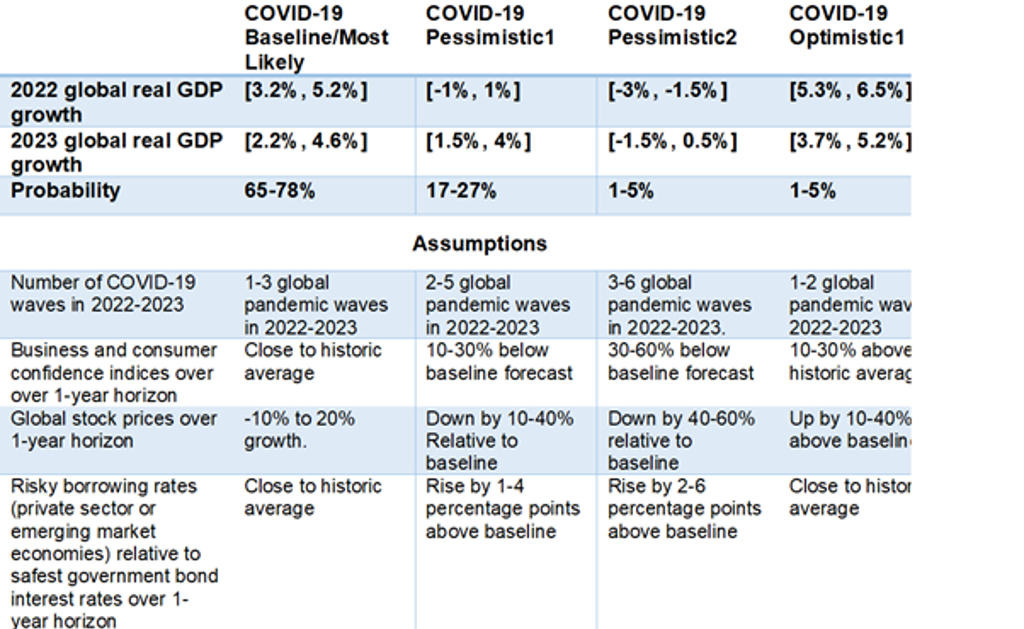

The baseline forecast assumes moderate negative economic effects of the current Omicron COVID-19 wave, mainly in Q1 2022. The existing vaccines remain highly effective against severe disease from new COVID-19 variants in 2022-2023, with moderate vaccine modifications. A combination of high vaccination rates and more widespread booster vaccinations, with significant extra immunity from infection with milder virus variants and greater availability of antiviral drugs, turns COVID-19 into an endemic disease in advanced economies by 2023.

Some social distancing precautions and occasional revaccination of more vulnerable groups are still necessary in 2022-2023 (especially in colder weather), but the global economic effects of COVID-19 remain moderate in the baseline scenario, equivalent to 0.2-1 percentage point reductions in annual real GDP growth rates. Many developing economies are unlikely to vaccinate the majority of their populations before 2023-2024 or even later; however, the growing tolerance of occasional spikes in COVID-19 cases and deaths is likely to moderate the economic effects of the virus. The baseline scenario is assigned a 65-78% probability in 2022.

Supply constraints continue to slow down the speed of economic recovery and raise inflation

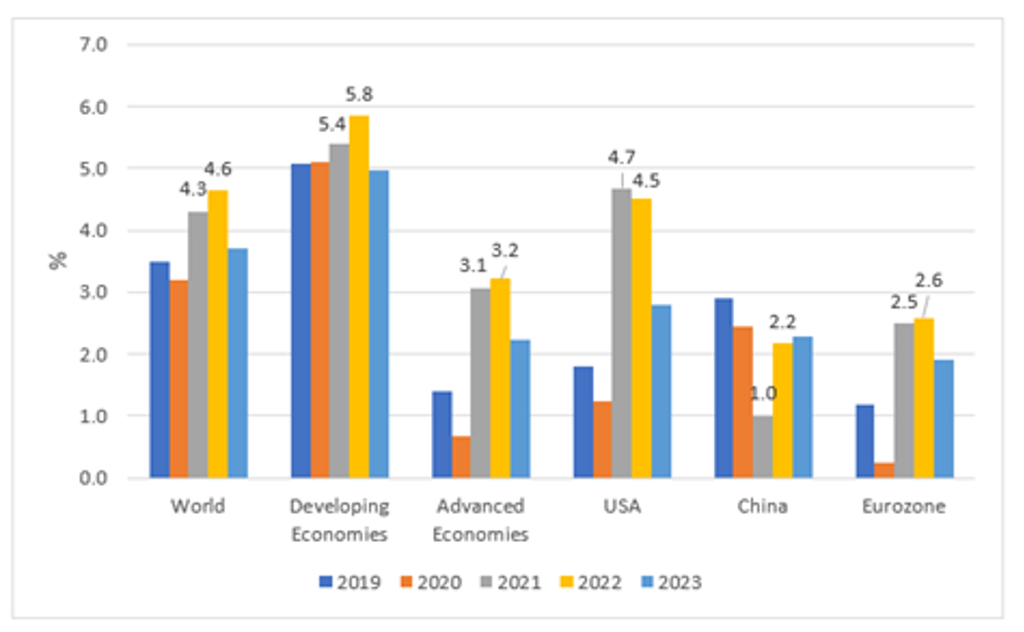

Global supply constraints remain substantial in Q1 2022, and they are now expected to diminish more gradually over 2022-2024 than in previous forecasts. Global consumer price inflation is estimated at 4.3% for 2021. Inflation is now expected to rise to 4.6% in 2022 (1 percentage point above the Q4 2021 forecast) and decline to a still relatively high 3.7% in 2023.

Inflation Baseline Forecasts: 2019-2023

Critical manufacturing sector inputs such as semiconductors continue to be in short supply, and worker shortages are ongoing in key sectors such as trucking, as well as food and hospitality services. Higher energy prices is one of the main factors in rising global inflation, especially in advanced economies, affecting the costs of both domestic electricity and heating as well as production costs for manufacturing goods. While global nominal wage growth has also increased, real wages after inflation have stagnated or declined in most countries in 2021.

Most of the supply bottlenecks and rising prices are related to an ongoing mismatch between the strong rebound in demand for goods and services in 2021, and the difficulties of ramping up supply chains and production after lower activity levels in 2020. However, the rise in expected inflation rates is partly self-fulfilling, with higher private sector inflation expectations directly contributing to higher price and wage increases to maintain profits and incomes.

The risk of war between Russia and Ukraine is also pushing the prices of oil and natural gas higher in early 2022. A Russian invasion of Ukraine could severely affect crucial gas supplies to Europe if Russia cuts supplies in retaliation for sanctions. In response, the US has set in motion plans for alternate gas supplies for European allies in case of war and cutbacks in Russian supply. Nevertheless, a Russian attack on Ukraine is likely to lead to another large increase in oil and gas prices.

Forecast risks remain tilted to the downside

Key global downside risks include new vaccine-resistant and highly contagious COVID-19 variants, stronger supply chain disruptions and energy price increases, as well as risks to financial stability in developing economies from rising global interest rates combined with rising debt levels during the pandemic.

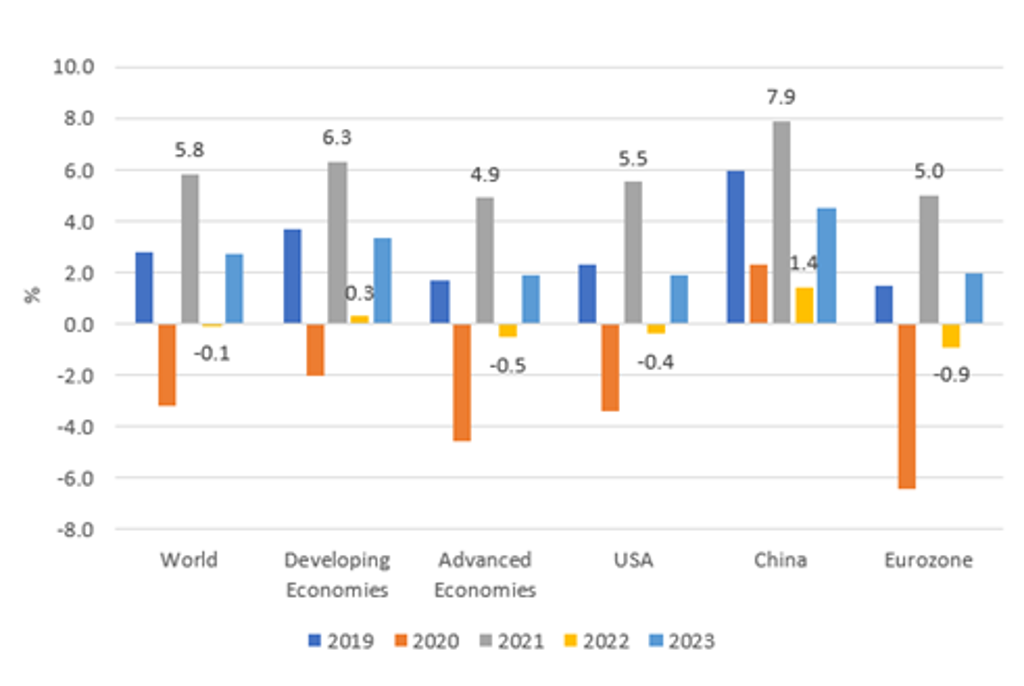

In the main COVID-19 Pessimistic 1 scenario, global real GDP growth is -1% to 1% in 2022 and 1.5-4% in 2023. The spread of a more infectious and highly vaccine-resistant COVID-19 mutation requires intense lockdowns and social distancing measures in 2022-2023, delaying economic recovery from the pandemic. The progress of vaccination campaigns in developing economies is slower than expected. The negative direct effects of the ongoing pandemic on economic activity are amplified by declining private sector confidence, rising uncertainty about the end of the pandemic, worsening financial market conditions and a more limited ability of governments to expand fiscal support measures. This pessimistic scenario is assigned a 17-27% probability in 2022.

Real GDP Growth COVID-19 Pessimistic1 Scenario: 2019-2023

COVID-19 Global Scenario Probabilities and Assumptions

For further insight, watch our webinar Global Economy in 2022: Getting Back on Track with Challenges Ahead.