Health and BeautyWe examine the trends underlying the growth of the global marketplace in health, beauty and hygiene. Our analysts will point the way forward by highlighting critical innovations and behaviours that are driving industry evolution.

As beauty and health products become more expensive due to high rates of inflation globally, consumers are forced to make more selective decisions when it comes to the products they buy. The result has been a polarisation of spending across the product categories. Private label brands are emerging as a significant alternative to balance consumer needs of efficacy and affordability.

High inflation intensifies recession concerns

Global inflation is forecast to reach 6.9% in 2023 which, while lower than the 2022 peak of 9%, is still high enough to have a significant impact on costs and purchasing power. Recession concerns have been intensifying in advanced economies as their growth outlook steadily worsened over the course of 2022. Economic data from the largest economies also indicate consumer savings as reserves accumulated during the pandemic helped to cushion inflationary effects and support consumption, the effects of which are forecast to wane in 2023, further exacerbating the issue.

The gap between current and constant growth widens in 2022

Growth in constant terms (which strips away the impact of inflation) is a tale of two cities. Beauty and personal care sales declined by 0.5% at constant 2022 prices in 2022, flattening from 3% growth in 2021 attributable to deceleration in the premium segment. High commodity prices and supply chain disruptions caused by the war in Ukraine and COVID-related shutdowns in China in 2022 set the global economy on a course of slower growth and high inflation. These factors negatively impacted retail sales (in constant terms) in several categories that were standouts the year prior, such as skin care and hair care.

Inflation causes decline in value in certain categories

The gap caused by inflation grew so wide in 2022 that retail sales globally in baby and child-specific products, bath and shower, depilatories and oral care also declined in real terms. However, these same categories registered positive growth in current terms, since they also happened to be categories that experienced steeper unit price hikes in 2022. Volume growth is an even more important metric in 2023 for the industry to understand how beauty consumers are coping with the cost-of-living crisis.

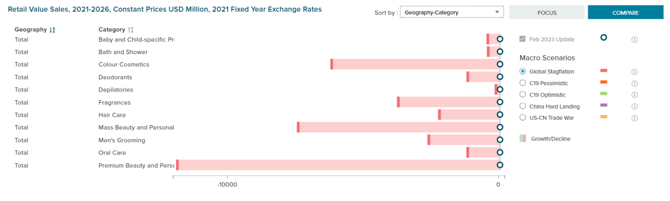

The scale of the impact on beauty and personal care categories over the forecast period (2021-2026) can been seen in the graph below, with a forecast negative impact on all beauty and personal care categories for retail sales in real terms.

Source: Euromonitor International Beauty and Personal Care Forecast Model, updated 31 October 2022

Beauty and personal care consumers look for alternatives as a result of rising unit prices

In other industries, like home and garden or food and drinks, consumers facing financial pressure turn to DIY solutions as a popular way of saving money. The chemical nature of many beauty and personal care products and the formulation inexperience of everyday consumers mean that this is not necessarily a feasible option. For example, misuse of cost-effective traditional remedies for hair loss like rosemary oil (which found popularity through social media platform TikTok in early 2023) has reportedly led to some consumers having ill effects such as hair loss and increased greasiness.

Instead, beauty consumers look to brands for products that will work as opposed to wasting money on unsuccessful experiments. They make concessions, look for alternatives and, in most cases, trade down in order to afford more premium products. However, the longer consumers face financial instability, the greater the need for companies to adopt strategies that resonate with cash-strapped consumers.

Greater demand for beauty and personal care products at affordable apparel retailer Primark comes as a result of consumers “trading down” to affordable brands, in order to allot resources to buy products that provide more of an indulgence (eg premium fragrances), or where price is perceived to correlate with efficacy (eg premium anti-agers). Source: Primark.com

Premiumisation through ingredient-led approach in mass tiers adds value

Brands are launching ranges with attributes often associated with premium products, but for a more affordable price. For example, Primark expanded its beauty and personal care division in summer 2022, launching a range of skin care products in partnership with Fairtrade, incorporating certified shea butter and olive oil, an attribute that would usually be associated with higher-cost products. Boots Walgreens in the UK announced in late 2022 a price freeze across 1,500 of its private label products, including the Boots Ingredient range, to directly address the cost-of-living crisis. In September 2022, the Boots Everyday range was launched and has since been expanded due to its success. Boots’ control over the supply chain means it can manage pricing more closely than other brands.

Private label growth to continue to accelerate

With high prices still a major concern, the acceleration of private label will be most noticeable in personal care categories. In 2022, 21% of consumers claimed they will increase their private label spend within the next five years, compared to 17% in 2021 (Euromonitor Voice of the Consumer: Beauty Survey, fielded in June 2022). In the same period (2022), 8% of respondents to Euromonitor’s Voice of the Industry: Beauty and Personal Care Survey said they have invested in their private label products as a direct response to inflation.

The higher level of control afforded by private label over price contributes to the correlation consumers need for convenience and budget efficacy in the face of financial hardship, and the growth of private label. The biggest challenge for the industry in 2023 and onwards is for specialist beauty companies to adopt a multifaceted approach to ensure consumer loyalty, while beauty consumers increasingly make trade-offs and shift their consumption to find the best intersection of value, efficacy and indulgence.

This report highlights key innovation trends in Consumer Health, analysing new product launch activity on e-commerce along with insights into key attributes and…

Marketplaces remain the cornerstone of FMCG e-commerce. However, their role is evolving as the broader digital commerce landscape becomes more fragmented and…

Amid a volatile environment shaped by geopolitical tensions and economic uncertainty, the eyewear industry is still poised for growth in 2026. Companies that…