Both Russia and Ukraine are important suppliers of commodities, agricultural goods and manufactured goods to the global economy. Russia’s invasion of Ukraine and resultant economic sanctions will have negative impacts on supply chains and are likely to impact a wide array of industries, ranging from food products to hi-tech goods. In addition, the invasion adds further pressure to the global logistics and transportation network. Below is a quick assessment of the impact on key industries.

Source: Euromonitor International

Energy prices forecast to increase

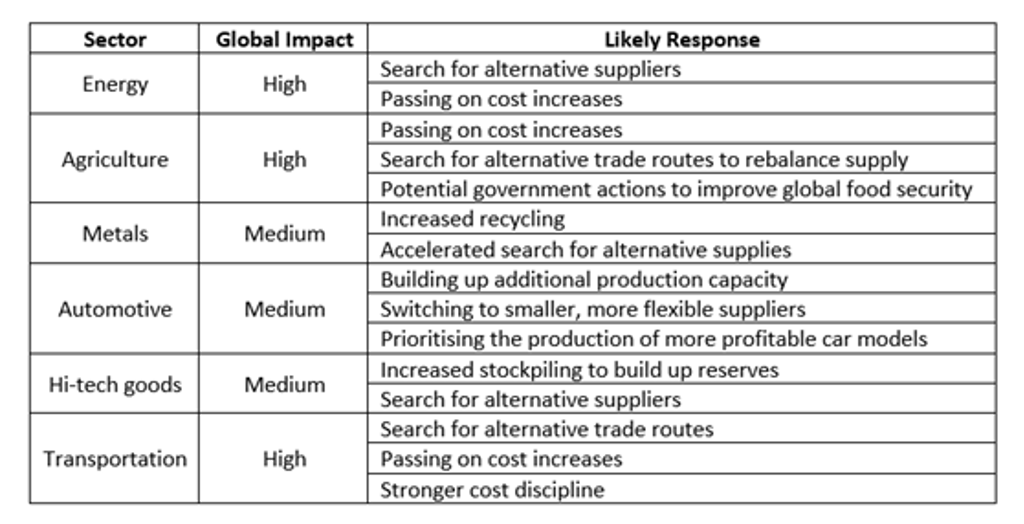

Russia is an important supplier of energy products, accounting for 12% of global oil supplies and 18% of global natural gas supplies as of 2021. However, European countries have higher exposure to Russian energy, as 40% of Russian oil and gas exports were destined for European markets in 2020. The invasion of Ukraine is expected to add more volatility to energy prices. Oil prices are forecast to remain above USD100 per barrel throughout 2022, while gas prices could rise by an additional 50% towards the end of the year. This would most heavily affect European companies with high energy intensity, such as those in metal and chemical products, fertilisers and other goods.

Financial sanctions on Russia and the worsened investment climate could also have longer-lasting negative effects on the energy industry. Several major oil companies, including BP, Exxon Mobil and Shell, have announced they are pulling out from the Russian market. This will impact new exploration projects and technological collaboration, in turn hurting long-term supply of energy resources.

Industries with the Highest Energy Intensity Globally, 2020

Disruptions to trade of agricultural commodities threaten global food supply

Ukraine and Russia are the breadbaskets of the world and among the key suppliers of food commodities. For example, Russia and Ukraine together supplied 15% of global wheat and 7% of rapeseed in 2021. Moreover, both countries are important suppliers of oils and fats used in food production, together supplying nearly 5% of global output in 2021.

The invasion threatens to disrupt agricultural commodity supplies, as reflected in the rising price of wheat and other commodities. For example, wheat prices have already soared by 70% in comparison with a year earlier. Higher prices of commodities will affect the global food and beverages sector, especially restaurants, animal feeds and ready meals, that use flour and oils and fats as input materials. Rising prices are likely to be passed on to end consumers and further add to inflationary pressures.

Constrained supplies of agricultural commodities also threaten global food security and will especially hit emerging markets in the Middle East, which import a large share of wheat from Russia and Ukraine. Moreover, transportation and trade disruptions could create large supply imbalances of agricultural goods. Food manufacturers are expected to diversify commodity supplies, and this will add more demand in regions outside of Europe. On the other hand, transportation problems in Ukraine could force commodity exporters to reroute supplies to alternative markets and create excess supplies.

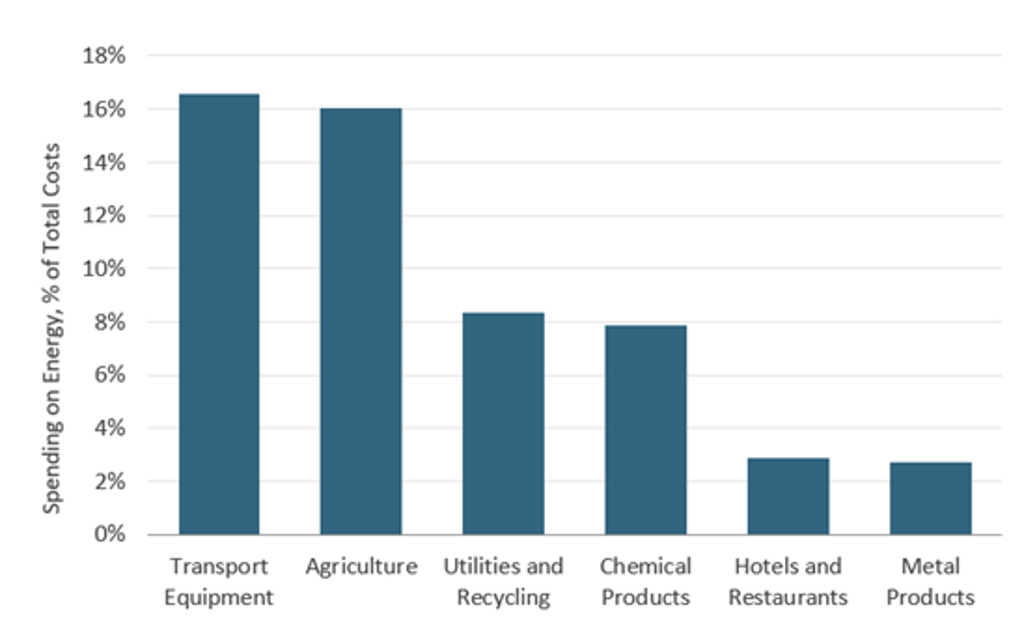

Industries with the Highest Global Spending on Grain Mill Products, Oils and Fats and Starches, 2020

Source: Euromonitor International from national statistics

Metal price increases threaten to hurt electric vehicle industry

Both Russia and Ukraine are important suppliers of metal ores and metal products. As of 2021, Russia and Ukraine together supplied 5% of the global crude steel and iron ore output and were among the key suppliers in Europe. The pause on metals production in Ukraine, transportation problems and fear over additional sanctions on Russian metals are inflating prices.

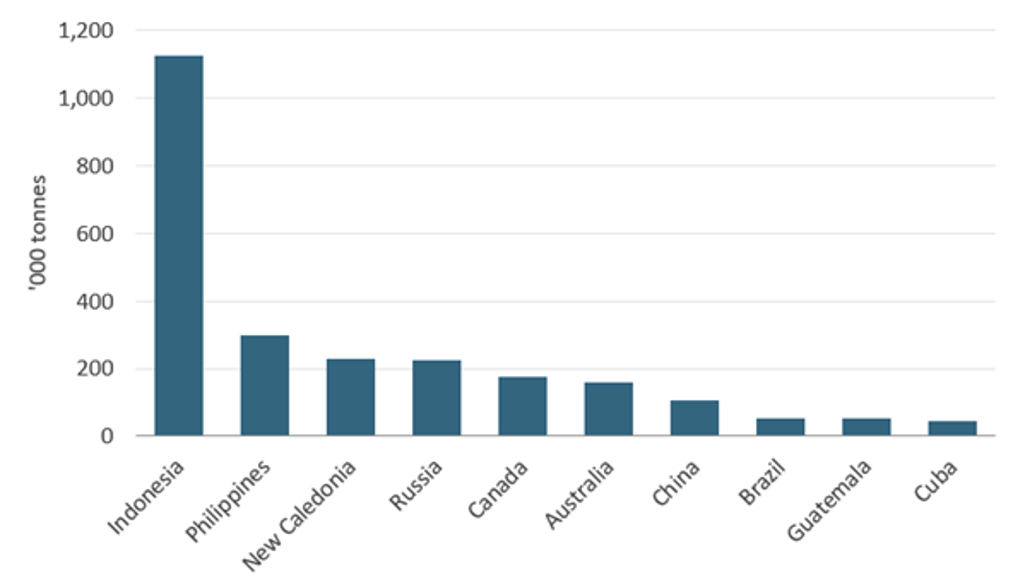

The invasion of Ukraine also threatens the global supply of nickel. Russia supplies around 8% of global nickel, which is key in producing stainless steel products and car batteries. Nickel traded at a record USD25,000 per tonne before trade was stopped at the London Metals Exchange to avoid further turbulence. The pressure on nickel prices is expected to remain, as companies fear additional sanctions on Russian exports and aim to stockpile more supplies. Further price increases could have a damaging impact on the battery industry and sales of electric vehicles.

Disruption to metals supply also has an effect on metals production outside of the European region. For example, US steel mills increased the prices of scrap by USD100 per tonne, as the supply of scrap metal from Russia and Ukraine ceased. Production disruptions may also have longer-lasting implications, as mining companies have indicated plans to temporarily pause investment projects, fearing that rising energy prices and inflation will hurt the demand for metal ores.

Largest Global Suppliers of Nickel, 2021

Source: Euromonitor International from US Geological Survey, British Geological Survey

Automotive industry to face additional component supply shortages

The automotive industry faces further supply chain disruptions due to the invasion of Ukraine. Ukraine is an important supplier of wiring and electronic components to European car manufacturers, and this will further add to the component supply problems. Total automotive exports from Ukraine stood at USD505 million in 2020 and accounted for 13% of the total production output. A shortage of wiring harnesses is the most immediate bottleneck, which could cause production delays for German car manufacturers. For example, Volkswagen has already halted the production of several electric vehicles due to disrupted supplies of wiring harnesses from Ukraine. Overall production disruptions could reduce European car output by 100,000 units in 2022.

Financial sanctions and the withdrawal of foreign car manufacturers from Russia will also impact the car industry, primarily European manufacturers. In 2021, more than 1.8 million new vehicles were sold in Russia. However, negative spill over effects to other markets are expected to be limited, as Russian automotive production was primarily destined for the domestic market, with exports accounting for 8% of total production.

Disruption of neon supplies impacts semiconductor industry

The invasion of Ukraine is forecast to have a negative impact on the global hi-tech goods industry, and semiconductors in particular. Estimates suggest that Russia and Ukraine together provide 50-70% of the world’s neon, which is used to run lasers to produce microchips. Neon comes as a by-product from the metals industry and production disruptions threaten the stability of the semiconductor industry’s supply chain.

Semiconductor supplies are expected to remain stable in the short term, as companies stockpiled neon and have reserves which will last from six weeks to three months. For example, the largest chip maker, Taiwan Semiconductor Manufacturing Co, announced it had accumulated neon supplies before the invasion of Ukraine. However, the long-term prospects for neon supplies remain uncertain. Substitutes may also be difficult to find in the short term, given the high shares held by Ukraine and Russia in the neon market. In case the disruptions are extended, the consumer electronics and industrial equipment industries would feel the heaviest impact from semiconductor shortages.

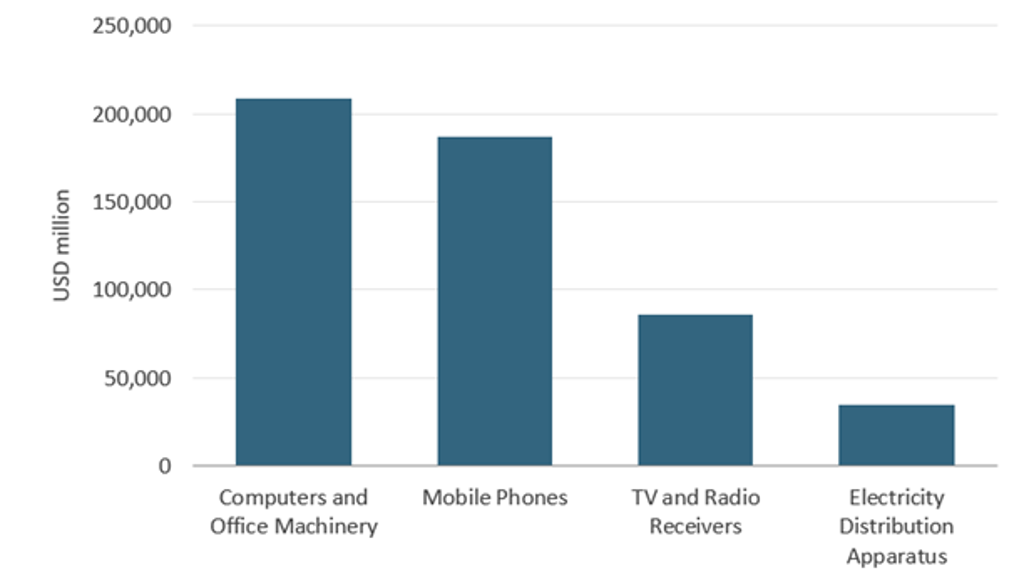

Industries with the Highest Global Spending on Electronic Components, Valves and Tubes, 2020

Source: Euromonitor International from national statistics

Transportation industry to face disruptions and rising costs

The transportation industry is expected to be among the most heavily affected. The invasion of Ukraine has disrupted land transportation and cut land routes between Europe and Asia. This will especially impact Chinese companies which use rail to transport goods to Europe. For example, the volume of goods carried by rail from China to Europe soared from 14 million metric tonnes in 2019 to 24 million metric tonnes in 2020, despite the pandemic. The invasion of Ukraine is expected to impact further growth.

Moreover, the closure of the Black Sea routes will disrupt global trade and will especially hit grain exports. Besides Russia and Ukraine, trade disruptions could also impact ports in Bulgaria and Romania. Lastly, the cutting of air ties between Europe and Russia (and in turn impacting routes to Asia) will impact the global airline industry. Disruption of air routes is also expected to impact the air cargo market and further inflate transportation costs.

Besides direct disruptions, the transportation industry will also feel a hit from rising energy prices. Expenditure on energy accounts for 13% of total costs in the transportation industry, thus transportation service providers will continue to feel inflationary pressure and will try to pass some of the increases on to end consumers.