This article is part of a series on the Coronavirus (COVID-19) focusing on how the outbreak is affecting industries, economies and consumers. Please note that these scenarios are accurate as of 29 September 2020.

Since June 2020, the global economy has recovered faster than expected from the effects of the first Coronavirus (COVID-19) wave. However, economic activity in most countries remains significantly below pre-pandemic levels and COVID-19 infection rates have increased in many countries since the summer, leading to new social distancing restrictions. Government financial support measures remain substantial but have been scaled back, constraining further recovery in consumer spending.

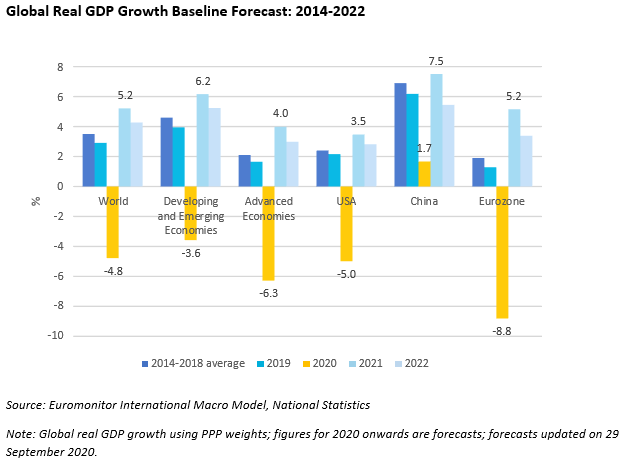

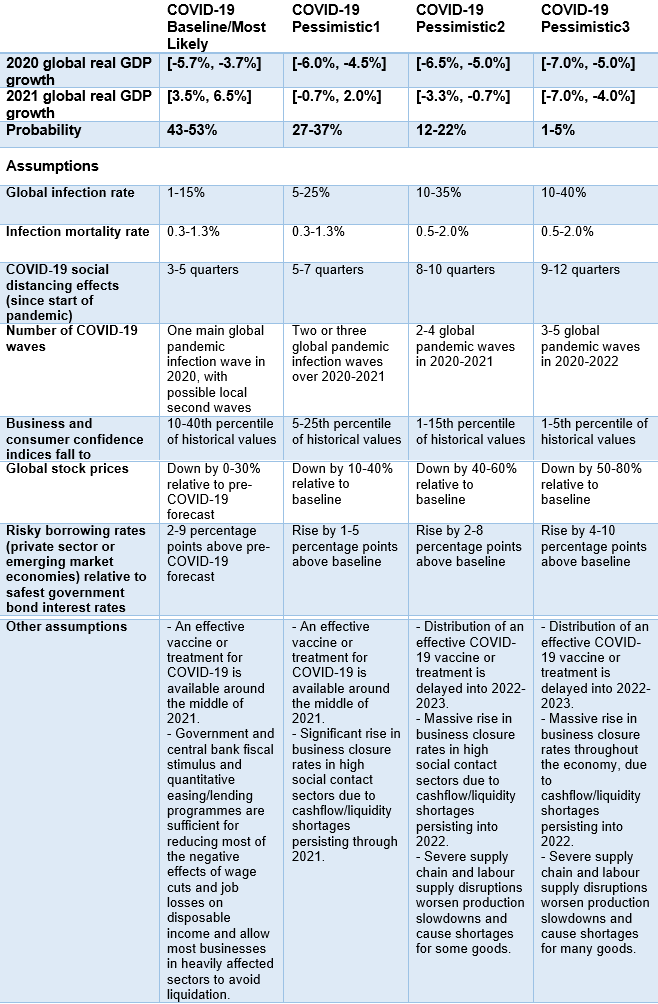

At the end of September, Euromonitor International updated its global macroeconomic forecasts. Global real GDP is still expected to contract by almost 5.0% in 2020 (a 3.7-5.7% decline), with a growth rebound above 5.0% in 2021 (with a plausible range of 3.5-6.5% growth). This would leave the global real output level in 2021 almost 6.0% below the pre-pandemic forecast.

The baseline forecast assumes that the major COVID-19 wave in Q1-Q3 2020 is followed by milder and better controlled regional second waves at the end of 2020. An effective vaccine for COVID-19 is expected to be available for widespread distribution around the middle of 2021.

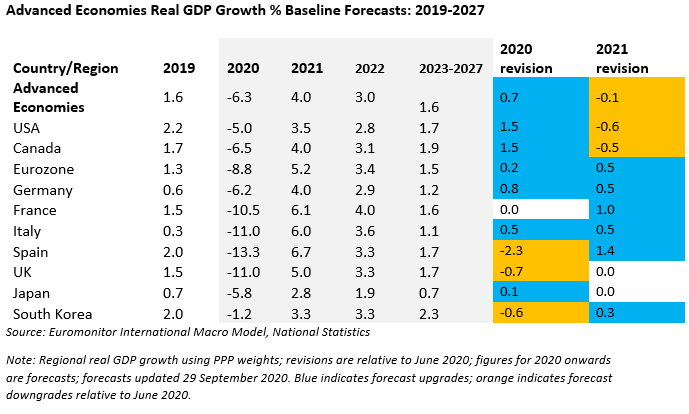

The global real GDP growth baseline forecast has remained stable since June 2020, but this reflects a combination of country specific upgrades countered by downgrades in other countries. Baseline forecasts have improved moderately for advanced economies due to faster than expected recoveries during the summer, with notable upgrades since mid-2020 to the US and Canada.

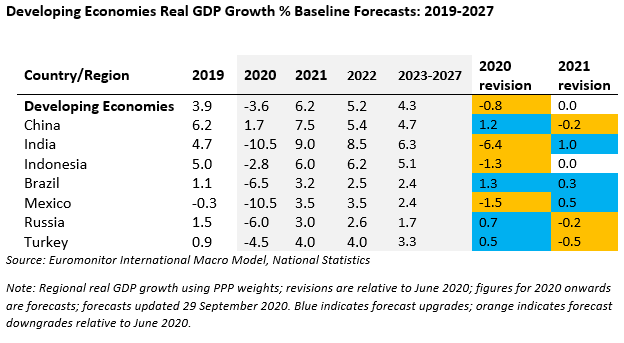

The aggregate developing economies real GDP growth forecast has deteriorated moderately, mainly due to the unprecedented contraction in India’s economy. In contrast, China’s economic outlook has improved, with real GDP growth for 2020 approaching 2.0% in our baseline forecast (compared to 0.5% growth in the June forecast).

Brazil’s forecast has also become more optimistic since the summer: real GDP is expected to contract by 6.5% (compared to an almost 8.0% decline in the June forecast) due to lower than expected social distancing restrictions and behaviours.

Global economic outlook remains tilted towards downside risks

The baseline/most likely outlook is only assigned around 48% probability (43-53%), with around 52% on our alternative COVID-19 pessimistic scenarios. The pandemic has worsened since the summer, especially in Europe, with short-term indicators signalling a slowdown or partial reversal of the economic recovery since mid-2020.

Risks of a severe economic hit from a second wave remain substantial in Q4 2020, with extremely high levels of uncertainty around the baseline forecasts. On a positive note, we have reduced probabilities assigned to the COVID-19 Pessimistic2 and Pessimistic3 scenarios that capture risks of delayed vaccine distribution to around 20%. This reflects reduced uncertainty about widespread availability of a COVID-19 vaccine around mid-2021.

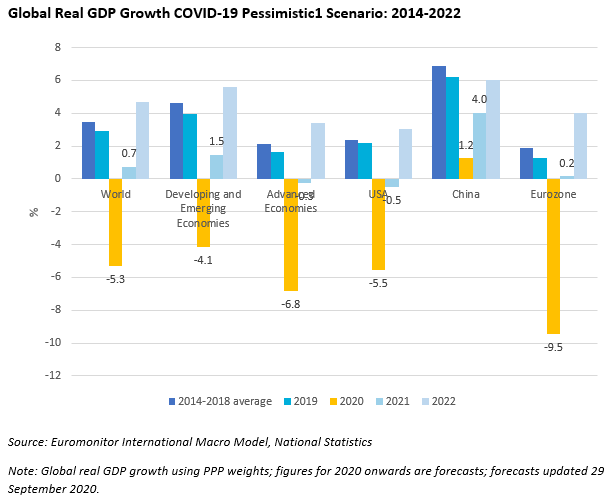

The COVID-19 Pessimistic1 scenario remains the most likely downside risk, with a probability of 27-37%. In this scenario, there is a major second global pandemic wave starting at the end of 2020, followed by a possible third wave in 2021. An effective vaccine or treatment for COVID-19 is available around the middle of 2021. 2020 global real GDP growth ranges from -6.0% to -4.5% in the Pessimistic1 scenario. The economic recovery is much weaker than in the baseline forecast, with global real GDP growth in 2021 ranging from -0.7% to 2.0%.

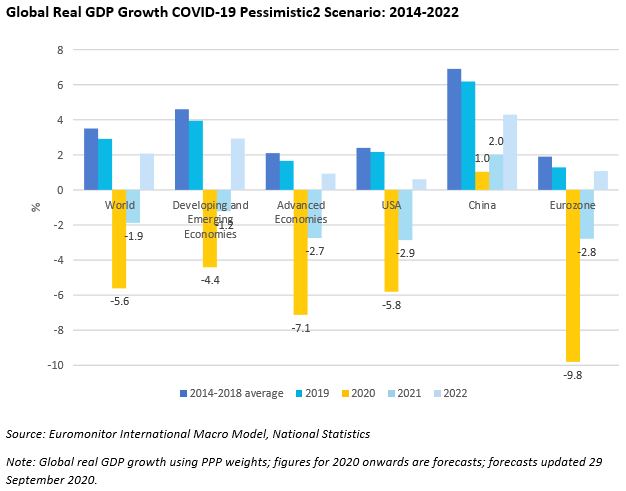

The main downside risk in terms of combined economic impact and probability is the COVID-19 Pessimistic2 scenario. In this scenario, the large-scale distribution of an effective COVID-19 vaccine is delayed into 2022-2023, leading to more prolonged social distancing effects. The second global pandemic wave starting at the end of 2020 is more severe than in the Pessimistic1 scenario, followed by a third and possible fourth possible waves in 2021. In this scenario, global real GDP contracts by 5.0-6.5% in 2020 and declines by a further 0.7-3.3% in 2021. This scenario is assigned a 12-22% probability.

Global economic outlook remains highly uncertain despite partial recovery

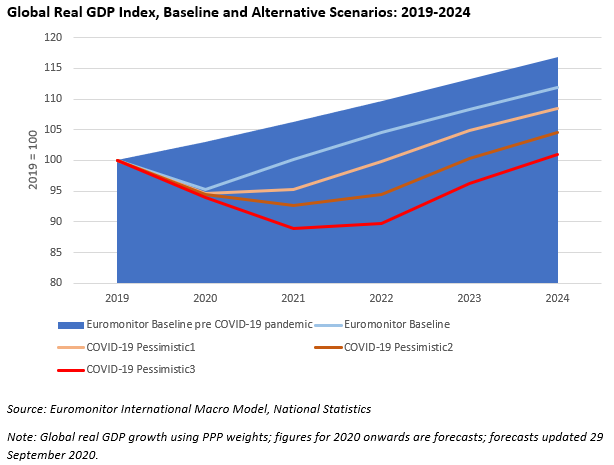

Economic recoveries from the bottom of COVID-19 lockdowns and social distancing have been faster than expected in many advanced economies, as well as China and Brazil. At the same time, other countries such as India and Spain have been affected worse than previously expected. The recoveries in Q3-Q4 are still likely to leave global economic activity in 2020 around 8% below the pre-COVID-19 forecast level.

As we enter Q4 2020, COVID-19 infection rates have increased substantially in many countries, signalling the emergence of a potential global second wave. Widespread adoption of face masks and other measures have made it easier to sustain economic activity while controlling the pandemic, making certain sectors like retail more robust. However, other sectors such as leisure, hospitality and tourism remain heavily depressed and vulnerable to a resurgence in the pandemic.

Governments’ fiscal support capacities have already been severely stretched in response to the first pandemic wave, leaving significantly less room for further fiscal stimulus in the case of a major second wave. On the upside, an unprecedented research and development effort is likely to lead to a vaccine being available for widespread use around mid-2021. However, the vaccine development and deployment processes are subject to major risks, leading to delays in availability into 2022-2023.

Under the baseline forecast, real global GDP growth rebounds by more than 5.0% in 2021, but this forecast is assigned only around 48% probability. Under the alternative pessimistic scenarios, economic recovery from mid-2020 is reversed and global real output remains severely depressed in 2021, potentially suffering another contraction. We assign these pessimistic scenarios around 52% probability, reflecting the unusual uncertainty surrounding forecasts during the COVID-19 pandemic. Click image for full size.

Notes: Social distancing effects include any substantial restrictions or private sector precautionary distancing, including, for example, 50% relaxation of full lockdown/quarantine conditions (eg limited store openings with restricted numbers of clients allowed, partial factory shifts), and ongoing consumer reluctance to frequent businesses in high social contact sectors (eg retail, food and drink services, entertainment services, tourism).

Significant global social distancing effects started in March 2020 with most governments not imposing lockdown measures before mid-March (end of Q1 2020). As an approximation, we start counting quarters of significant social distancing in Q2 2020.

Scenarios start in Q4 2020. This takes into account uncertainty about the current situation in Q4.