The outlook for the global economy remains challenging, as the war in Ukraine lingers and private consumption shows signs of weakening amid intensified inflationary pressures and rising uncertainty.

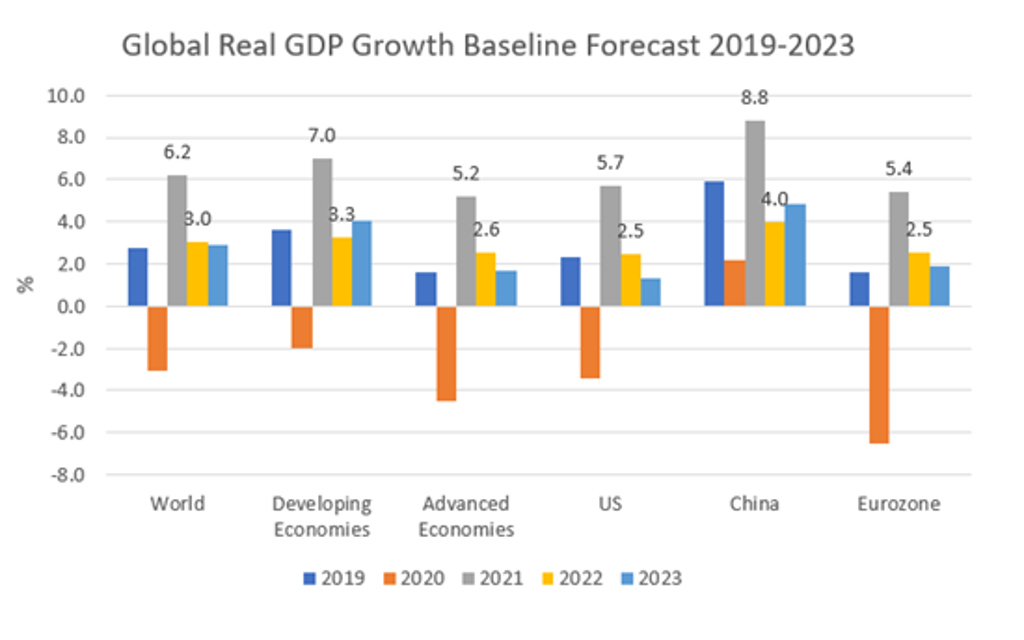

Global real GDP growth is expected to slow significantly from a strong recovery of 6.2% in 2021 to 3.0% in 2022 and 2.9% in 2023 in Euromonitor International’s Q3 2022 baseline forecasts.

Inflation is projected to surge further in many key economies as a result of ongoing increases in food and energy prices, curbing real incomes and consumer spending and further dampening the global growth outlook. The risk of global stagflation remains significant.

Economic growth weaker than expected in key economies

High commodity prices and supply chain disruptions caused by the war in Ukraine and shutdowns in China amid its zero-COVID policy continue to set the global economy on a course of slower growth and high inflation. Global economic performance was rather resilient in the first quarter of 2022 but has weakened significantly since the second quarter as the impact of the war started to play out. While economic performance in some emerging markets including India and Brazil improved, growth in some key economies including the US and China has been weaker than expected during the second quarter of 2022.

Global real GDP growth rates for 2022-2023 are slightly lower than Q2 predictions at 3.0% in 2022 and 2.9% in 2023, according to Euromonitor International’s Q3 2022 baseline.

Note: (1) Data from 2022 are forecasts; forecasts updated 4 July 2022 (2) Regional real GDP growth using PPP weights

European economies continue to be hit hard by the impact of the war in Ukraine, given its high exposure through energy imports. Russia announced further energy supply cuts to Europe in July 2022, making the risk of an energy crisis gloomier and prompting the EU to agree on an emergency plan to curb gas demand. Although a strong labour market and accumulated household savings are still supporting growth in the eurozone, rising energy prices, growing uncertainties and weakening external demand will weigh on the region’s economic outlook.

In Euromonitor International’s Q3 2022 baseline scenario, 2022 and 2023 real GDP growth forecasts for several eurozone economies, including Germany and Italy, were revised downward.

The eurozone as a whole is now predicted to grow by 2.5% in 2022 and by 1.9% in 2023, compared to growth of 5.4% recorded in 2021.

For the US, 2022 real GDP growth forecast was revised downward by a 0.5 percentage point relative to previous forecasts to reach 2.5%. US consumer confidence has weakened further, with a renewed decline in June 2022, as pent-up demand is fading and high inflation is affecting consumer purchasing power.

For 2023, Euromonitor International predicts the US economy will grow by 1.5%, representing a 0.5 percentage point downward revision from its Q2 2022 forecast.

China’s economic slowdown has also been more significant than expected, driven by lower consumption and disrupted activities as the country retains its zero-COVID policy. China’s official manufacturing purchasing managers index fell to 49.0 in June 2022, below the 50-mark that indicates a contraction in activity. Problems in the Chinese real estate sector continue to damage property investment and sales, dragging down economic growth. China’s economy is expected to grow by 4.0% in 2022, before it improves to approximately 4.8% in 2023.

High inflation threatens a cost of living crisis

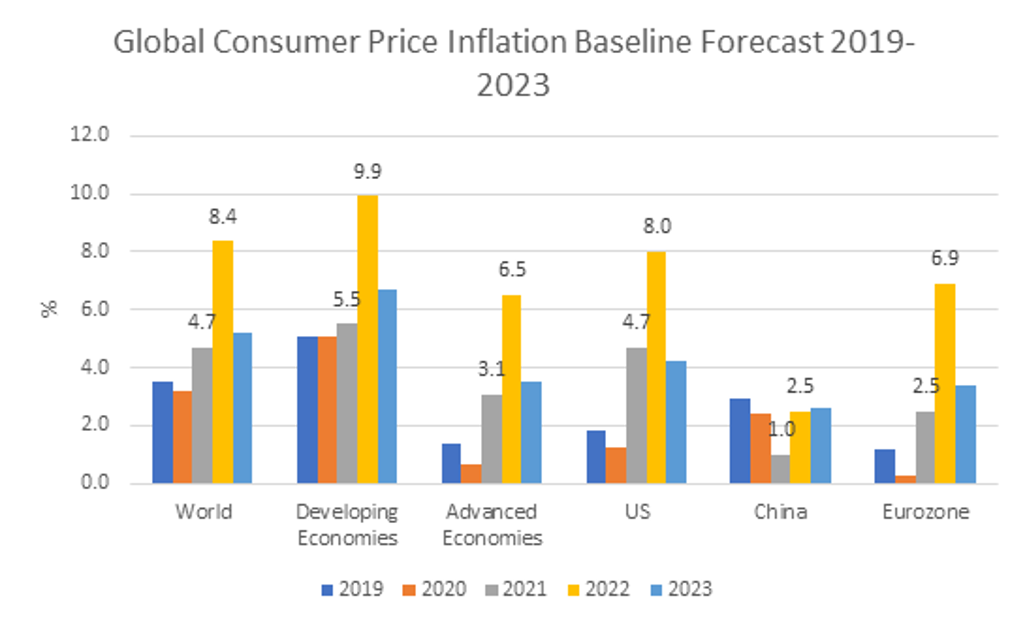

Inflationary pressures continue to rise as countries worldwide are hit by persisting problems in the supply chain and rising commodities prices. Euromonitor International’s 2022-2023 inflation forecasts were revised upward for most key countries in Q3 2022 relative to predictions made in the last quarter. Inflation is now expected to reach 9.9% in emerging and developing markets and 6.5% in advanced economies this year and will likely stay above trend next year.

Source: Euromonitor International Macro Model

Note: (1) Inflation refers to consumer price inflation measured by consumer price index (CPI) (2) Data from 2022 are forecasts; forecasts updated 4 July 2022 (3) Regional real GDP growth using PPP weights

Following the onset of the war in Ukraine, the global energy and food price index increased by 86.0% and 27.0% year-on-year respectively, and reached a record new high in the second quarter of 2022. This will particularly hurt low-income markets which are dependent on energy and food imports and could trigger social unrest and tensions in these countries.

Across economies, rising prices are undermining real income growth and could force households, especially among lower- and middle-income groups, to reduce their spending amid the risk of a cost of living crisis. Given the intensified inflationary pressures, many central banks worldwide have increased their interest rates to tame high inflation. Tighter global financial conditions could result in financial distress for emerging and developing markets, further affecting the global economic outlook.

Downside risks still dominate

Source: Euromonitor International Macro Model

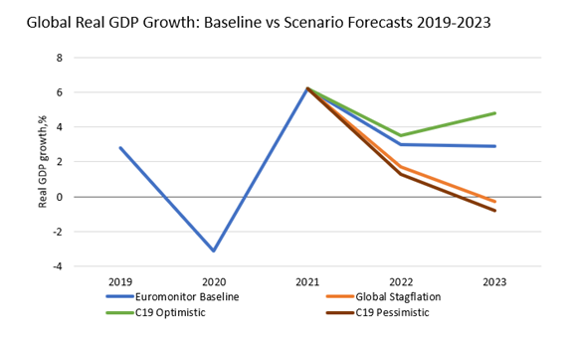

Note: (1) Data from 2022 are forecasts; Data updated 4 July 2022 (2) Regional real GDP growth using PPP weights (3) Scenario probability over a 1-year horizon: Global Stagflation 27%; C19 Pessimistic: 18%; C19 Optimistic: 3%.

The global economy continues to face growing uncertainty, with global stagflation remaining the main downside risk. More abrupt cuts in Russia’s gas supply to Europe and an intensification of the war in Ukraine could make it more difficult to bring down inflation, while affecting production and damaging business and consumer confidence. The US and eurozone economies are facing high stagflation risks, but developing and emerging markets could be hit hard if the global economy enters a stagflation era. Meanwhile, renewed COVID-19 outbreaks or the emergence of a new highly infectious variant remain a risk, which could again disrupt economic activities and suppress global growth.

Find out more about the risks and likely scenarios for the upcoming year in our full report, Global Economic Forecast: Q3 2022.