Consumers in the US developed a renewed focus on healthy eating habits during the COVID-19 pandemic. Despite the resumption of eating out, the focus on healthy eating has persisted, and the blender has become the appliance of choice for food preparation at home. Blenders is expected to grow by a CAGR of 3.4% from 2021 to 2026 – a relatively high growth rate for a mature category.

Via, Euromonitor International’s e-commerce tracking tool for online prices, availability and ratings for stock keeping units (SKUs), can easily identify trends in the market and provide strategic and tactical recommendations. In this piece, we will take a granular look at how blenders have performed at the US’s largest electronics and appliance specialist retailer, Best Buy, to understand:

- How have prices fared in the first half of 2022 by category and supplier?

- How do price changes compare by pricing tiers?

- What is the relationship between prices and online ratings?

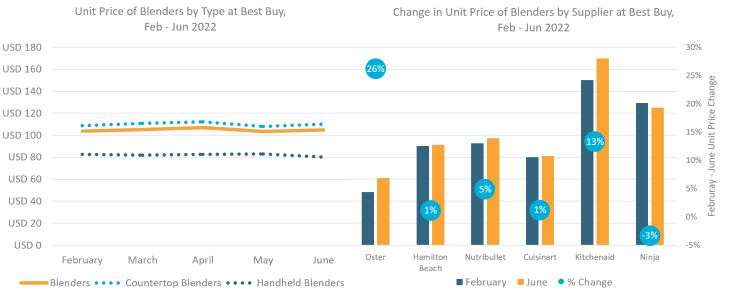

Suppliers’ price changes differ significantly from category averages

Note: Leading brands selected based on combination of brand share and SKU availability, Blenders SKU Sample, N=70

- Within this sample of blender SKUs at Best Buy in the US, prices in the category (seen on the left) largely held consistent during the five-month period February to June, with an increase of just 0.8% to reach USD104.67. However, breaking out the different types of blenders showed more variance in pricing pressures. Prices of handheld blenders declined by 3.0% during this time period, as suppliers as well as their retail partners, in this case Best Buy, were looking to find additional ways to encourage consumers to purchase these discretionary goods, given the inflationary pressures consumers were feeling in other categories. Furthermore, in the early part of the second quarter of the year, many retailers and suppliers in consumer appliances were looking to move excess inventory that had built up as a result of a dynamic variance in supply and demand, also known as the bullwhip effect.

- Analysing how prices changed at this retailer at the brand level shows more significant changes in prices and strategies. The leading three brands by retail sales (Newell Brands’s Oster, Hamilton Beach, and De’Longhi’s Nutribullet) all showed price increases; however, the lower-priced Oster brand showed the strongest price increase over this period. Lower-priced products in particular feel the strongest impact of inflationary pressure, and often need to increase prices to offset disproportionate increases in component and energy costs. Meanwhile, one of the fastest growing brands in blenders, Sharkninja’s Ninja, saw a decrease in prices. The company enjoys strong margins, and here we can see that aggressively dropping prices against its competitors can provide a key opportunity to attract customers in such a challenging economic environment where prices are rising. Given the severe swings in demand and the lag time in procuring supplies for manufacturers, tracking price increases at the individual retailer level can give strong insights into how competitors’ prices are faring compared with one’s own.

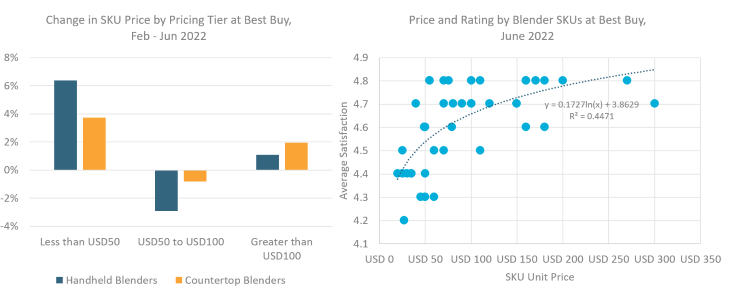

Consumers value higher-priced blenders, up to a point

Note: Leading brands selected based on combination of brand share and SKU availability, Blenders SKU Sample, N=70

- Analysing this sample for Best Buy by pricing tiers can give insights into how the prices of different SKUs are impacted by their price positioning. Within blenders, on the left chart, we can see that lower-priced products, that are priced at less than USD50, saw the largest price increases, for similar reasons as stated above for leading brand Oster. This can present a variety of problems for suppliers, as price increases in this pricing tier put further inflationary pressures on less affluent consumers looking to purchase more affordable blenders. However, as can be seen in the middle pricing tier, products priced USD50 to USD100, prices in this range declined, so this presents an opportunity for mid- to higher-priced models to attract consumers who are perhaps willing to trade up to a more premium product, given the reduced gap in price between models.

- On the right chart, one can see how individual SKUs perform from a pricing versus consumer satisfaction level, based on online self-reported ratings on Best Buy’s website. Including SKUs that had at least 50 online reviews, there is a clear relationship between the average price of the model and consumers’ self-reported satisfaction, up to a point of around USD100, indicating consumers do typically feel they are receiving additional value for every extra dollar spent on these products. However, for the more premium models satisfaction levels can vary, and this indicates the elevated expectations consumers have for these higher-priced products. Understanding this relationship between price and satisfaction provides suppliers and retailers with additional price-setting information and direction, particularly as companies look to vary pricing strategies to deal with supply chain management alongside consumers’ inflationary concerns.

As consumers and companies struggle to adjust to new inflationary pressures, monitoring online prices, availability and ratings for selected categories and baskets of goods provides key insights into how price increases are manifesting themselves and how consumers are reacting to these changes. While this piece looked at an individual retailer, Via covers over 2,000 online retailers in 80 countries in 11 consumer goods industries. Learn more about how Via can support your business and help you unlock key strategic and tactical insights with its standardised online product coverage.

Note: Sample based on SKU prices found in Euromonitor International’s e-commerce tracking tool Via, with data extracted in August 2022. Please note that due to ongoing improvements to the AI-led product matching of SKUs to categories, suppliers and brands, data and SKU counts can be revised based on system updates. SKU counts used for the analysis from Best Buy on selected dates to represent monthly figures, N= 70.

To request a demo of Via, get in touch.