According to Euromonitor International’s recently released COVID-19 themes, ‘the arrival of COVID-19 accelerates trends, such as the rise of online, click & collect, frictionless retail and D2C’. The pandemic has been a pressure test for e-commerce infrastructures, with some markets faring more resilient than others. To better diagnose what markets are more prepared for this ‘new normal’, it is important to discover if there is a causal relationship between the number of COVID-19 cases and online product availability to illustrate the level of preparedness of suppliers and online retailers.

Using our Price and Availability Tracker technology, we are able to measure total percentage out of stock (%OOS) across an online basket of essential consumer goods categories spanning 10 industries, including non-alcoholic drinks, packaged food, tissue and hygiene, consumer health, beauty and personal care and home care. For this analysis, we will examine how %OOS changes alongside changes in reported COVID-19 cases, with a 2-day lag to account for the reactive nature of consumer behaviour.

Overreliance on brick and mortar?

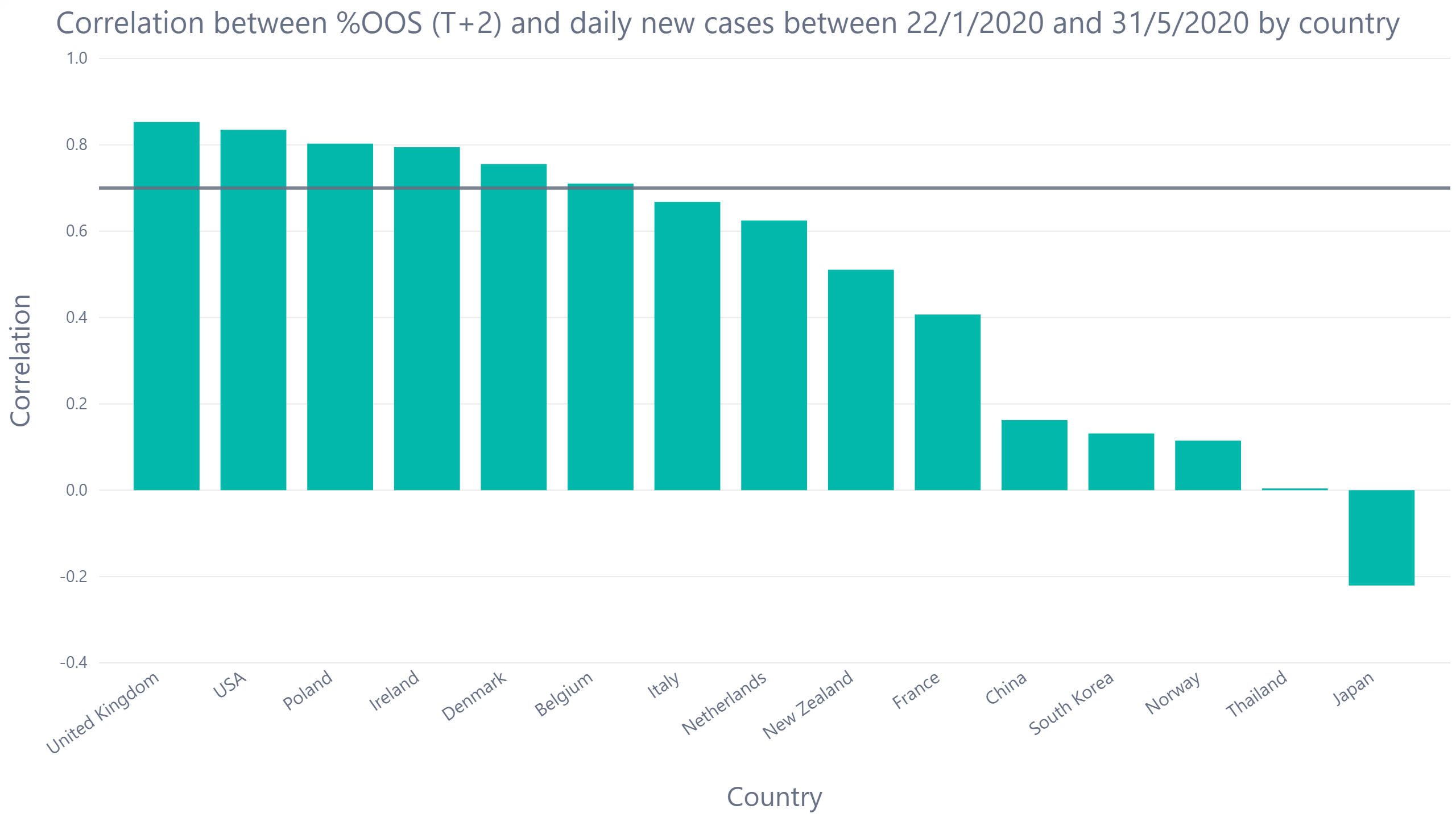

Take United Kingdom for example, the correlation value for UK is just above 0.8, which is considered a relatively high value. This implies that when COVID-19 reported cases rose, the %OOS similarly rose 2 days later. In other countries such as USA, Poland, Ireland and Denmark, %OOS is also highly correlated to the number of cases two days prior.

Fig.1 Correlation between %OOS and daily new cases between observation period

The factor in common for these countries is that they still rely significantly on brick and mortar retailers. According to Euromonitor Passport data, as of 2019, 80% of the retail sales are through store-based retailers in the UK, US and Poland, with Ireland reaching 90%. Since countries were in lockdown and social distancing practices have reduced abilities for consumers to shop in-store, consumers turned to online retailers. The e-commerce structure cannot restock quick enough to handle the sudden surge of demand, which lead to a high %OOS.

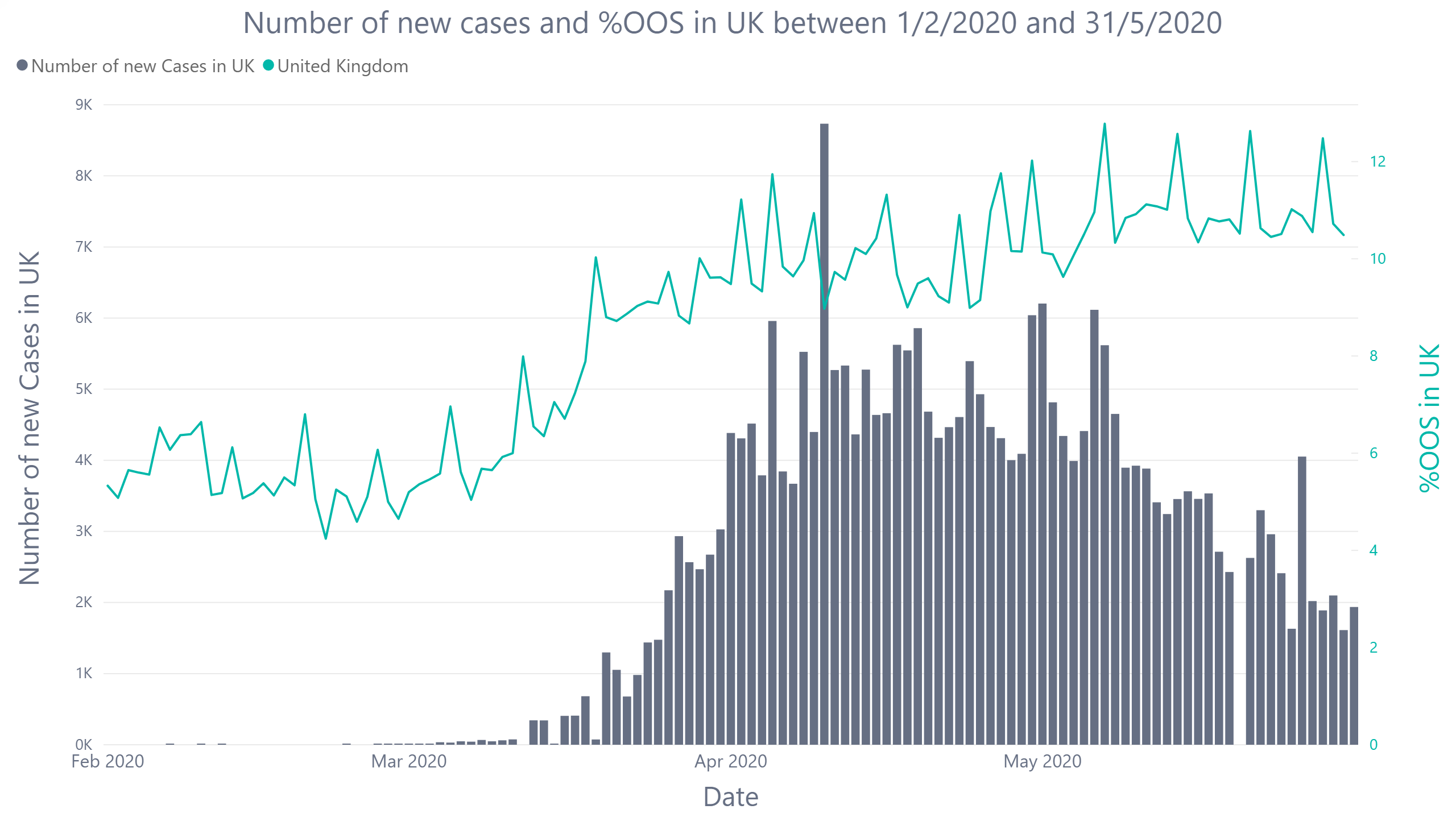

Fig.2 Comparison between number of daily new cases and %OOS of UK online retailers

In early May, OOS% in the UK reached about 12% as reported COVID-19 cases surged, meaning 1 in 10 essential consumer products were out of stock. In Ireland, the ratio was even more extreme, with 1 in 5 essential consumer goods out of stock. The fundamental purchasing pattern of consumers is likely to remain after the pandemic settles, and these countries will have to improve their e-commerce infrastructure to adapt to the new consumption pattern.

Meeting new shopper needs

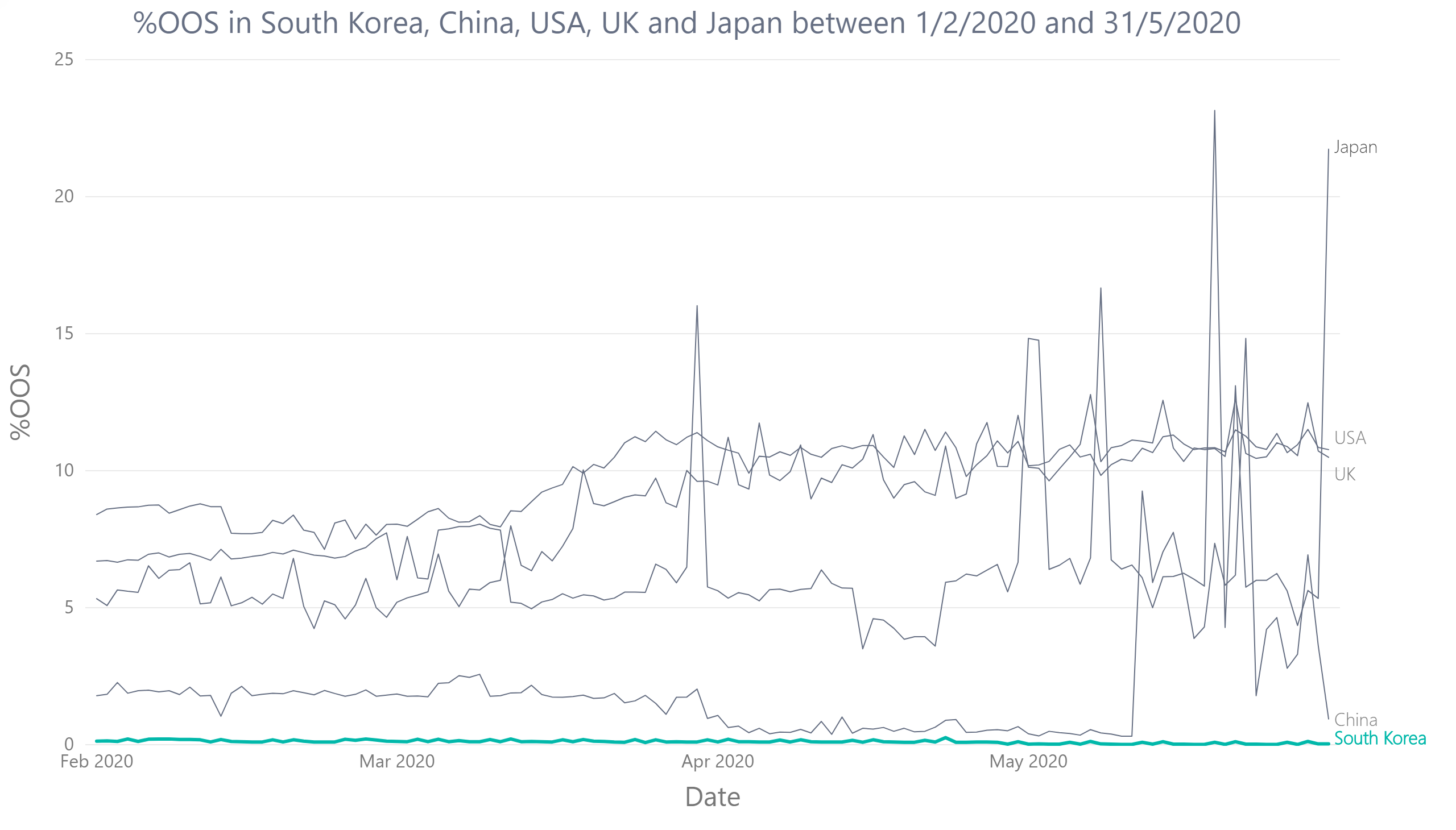

On the other end of the spectrum, there are countries that are faring well from a stock availability perspective. South Korea had the lowest %OOS over their outbreak period and had no significant correlation with the number of new cases. From a %OOS point of view, South Korea never broke more than 1%OOS, while the other countries, like Japan, the US, UK and China, varied significantly over time.

Fig.3 %OOS of South Korean online retailers against other countries

According to Euromonitor Passport, nearly 30% of South Korea’s total retail revenue was generated through e-commerce in 2019. This staggering statistic was achieved with the help of two important factors: delivery efficiency and competition.

Fig.4 Online retail sales proportion

Euromonitor research manager in the South Korea office Jamie Ko stated that most online retailers offered one-day delivery, and many offered same-day grocery delivery on orders placed before noon, standardising the convenience over in-store shopping regardless of the retailer.

The e-commerce scene is also very competitive within South Korea. The fierce competition between e-commerce market operators and third-party operators has resulted in additional benefits for the consumer, with perks such as loyalty programs, promotions and low delivery costs.

In conclusion, the outbreak of COVID-19 has tested the durability of e-commerce and delivery infrastructures around the world and shown whether a country is ready for the ‘new normal’ online consumption habits.

Our correlation analysis shows how shock absorbent an e-commerce infrastructure is from a product availability standpoint, with some countries unable to handle the sudden surge of online orders and others only mildly affected by the outbreak as those consumers were already accustomed to shopping online. In order to be ready for the new normal, retailers in countries struggling with product availability should look to countries that were able to keep out of stock rates down, like South Korea and China.

Online retailers will need to work with private and government stakeholders to develop solutions for post-COVID-19 shopping behaviours. This may mean introducing more competition into the e-commerce ecosystem, improving delivery systems and fulfilment models, or even subsidising e-commerce operators all with the aim to develop a more robust e-commerce infrastructure.