Food and NutritionConsumers are engaging with food and nutrition like never before. Our in-depth analysis examines the most important implications across the industry, providing market intelligence, original thinking and key insights.

The COVID-19 pandemic rapidly changed consumers’ behaviour and gave a shock to fmcg industries in 2020/2021. The road to recovery in 2022 has been hindered by spectacular inflation globally, and the war in Ukraine. With growing prices of energy, commodities, and end products, many consumers’ financial stability is more vulnerable than ever before. This raises attention to cost-saving solutions, with private label coming into focus. However, modern shoppers have demanding expectations of the products they buy, which has driven the transformation of private label and, in turn, changed perceptions.

Consumers slow to change spending habits – but it is happening

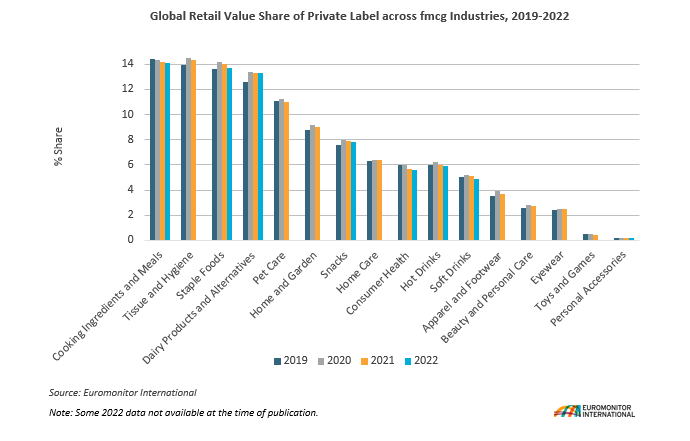

In 2020, the first year of the COVID-19 pandemic, private label saw a tangible rise across most fmcg industries. This was followed by branded offerings taking back ground in 2021 and the first half of 2022, when COVID-19 restrictions eased, and consumer confidence rose. The inflation surge started in mid-2021, and was exacerbated by Russia’s invasion of Ukraine, but consumers’ desire to travel, go out, and purchase more brands (revenge consumption after COVID-19) delayed their reaction to price hikes, which has not favoured the development of private label in 2022. However, with prices reaching new heights and consumer demand for value for money offerings, 2023 could be a favourable year for retailers’ own brands.

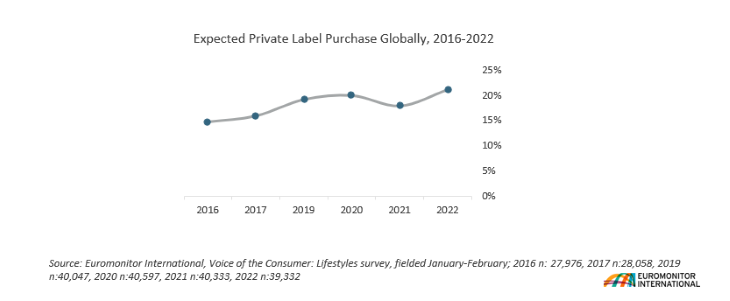

The expectation of private label growth is noted by both industry players and consumers. According to Euromonitor International’s Voice of the Consumer: Lifestyles survey, fielded January to February 2022, 21% of all respondents globally are planning to increase their purchases of private label products in the next 12 month period. This is the highest level recorded over the last six years. In October-November 2021, 65% of industry professionals surveyed as part of Euromonitor’s Voice of the Industry: Lifestyles survey 2021, expected that consumers will increase their visits to discounters, and 56% said consumers will increase their purchases of private label goods. Private label products have a strong presence in discounters, and in countries where discounters have strong penetration, private label has the highest share. Countries in which the penetration of discounters is growing the fastest generate the highest growth for private label.

Private label has moved beyond “basic”

As private label lines have become significant market players alongside brands, they have tended to transform and serve consumers with more than just basic needs. Penetrating different consumer groups, private label lines aim to play within the economy, standard and premium segments. Retailers do not only change the appearance and ingredients of the products, but also enter very small and sometimes experimental segments.

Thus, these times of uncertainty do not necessarily solely mean the rise of budget solutions, but also pave the way for premium private label products as better-priced alternatives to branded goods. Private label options allow consumers to enter premium, niche categories without compromising their spending. This growth enables retailers’ private label lines to build consumers’ awareness within categories where it is low.

Consumers give the direction

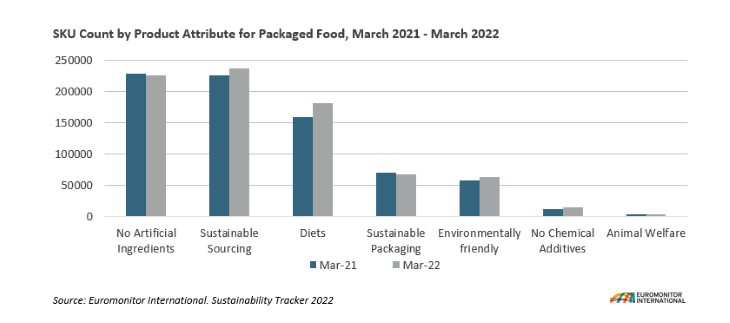

To remain competitive, private label products always look at and sometimes copycat the strategies of leading brands. Branded products continue to invest in the development of solutions targeting specific needs: more SKUs of packaged food which include claims such as Vegan, Vegetarian, Plant-based, etc. are appearing within e-commerce. According to Euromonitor’s Sustainable Living Tracker, the number of SKUs with the attribute of Diets (including the claims mentioned above) increased by 14% in March 2022 compared with the same period the previous year.

Healthy living informs private label development

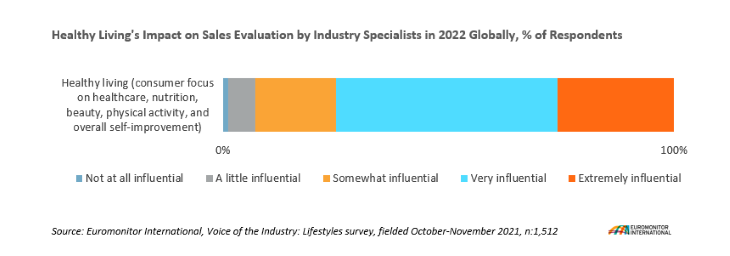

Euromonitor International’s Voice of the Industry: Lifestyles survey 2021 also reveals that industry professionals consider healthy living to be the factor which will most impact sales within the next 12 months. 93% of those surveyed globally think the importance of this will vary from somewhat to extremely influential.

As it has become obvious that health awareness cannot be omitted within the evolution of private label, retailers have responded. A clear example is Carrefour Polska’s 2022 launch of the vegan product Sensation Vegetal, for consumers who not only prioritise healthy living, but also care about animal welfare and local origin (the product is sourced from Polish suppliers). The packaging highlights all the benefits of the product, which are in line with the opinions expressed by consumers in Euromonitor International’s Voice of the Consumer: Health and Nutrition/Lifestyles surveys.

Free from preservatives: 34.5% of surveyed respondents name this attribute as important in their dietary preference in 2022.

Vegan: 8% of consumers say vegan is important in their dietary preferences in 2022.

Contains fibre: 25% say that containing fibre is important, and 68% of these respondents look for it for the reason of digestive health in 2022.

Nutrition score: in 2022, 53% look for healthy ingredients in foods and beverages. This labelling is a quick and catchy way to compare one product with another.

Carrefour Sensations: Does not replicate the name of the store; however, uses the logo, therefore forms stronger loyalty with the chain.

Private label adapts to changing consumer demand, be it a surge in demand for budget solutions, or requests for something beyond the standard. Retailers will continue to manoeuvre within the set of different price-tier solutions to shield from competitors and increase the loyalty and trust of shoppers. More premium private label products will be developed to enter various niches.

Energy management is reshaping coffee consumption as consumers seek more control over caffeine, focus and wellbeing across the day. Coffee risks losing key…

Marketplaces remain the cornerstone of FMCG e-commerce. However, their role is evolving as the broader digital commerce landscape becomes more fragmented and…

This report examines how leading companies are shaping strategies in challenging times. Chief amongst the headwinds they face is a continued difficult consumer…