Even before the pandemic, Latin America was a region affected by socioeconomic crises in many countries. The pandemic has inevitably compounded this, particularly for non-essential service industries, where consumer foodservice can be a relative extravagance, susceptible to reduced spending.

In 2021, consumers have resumed visiting restaurants, following the lifting of social distancing restrictions and mass home seclusion. But with ongoing economic problems and surging inflation, consumers are more cautious in their spending, with many opting for cheaper meals, a consideration which is delaying more rapid industry recovery. Fast recovery in Chile is both an indicator of potential growth and prescient warning, with implications for Latin America and the consumer foodservice industry overall.

Resilient market performance in Chile

Chile’s foodservice industry is set to see the fastest recovery in Latin America, reaching 2019 market value levels in constant terms by 2023. The high vaccination rate and uptake of booster shots have seen widespread resumption of social activities, including foodservice. Chile also approved the withdrawal of a percentage of retirement funds during 2020 and 2021, which allowed for market liquidity and a financial bubble for consumer confidence, which reactivated expenditure.

These milestones underpin Chile’s resilience, but there are additional factors which make this foodservice market stand out compared to the rest of Latin America.

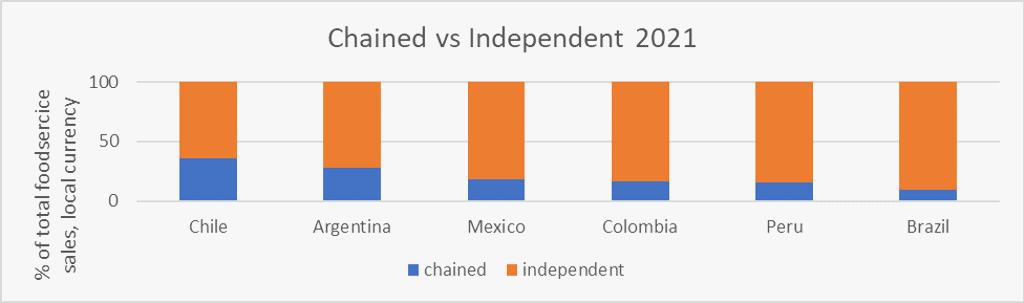

Market fragmentation risks slower recovery

Latin America is characterised by high fragmentation, with many independent restaurant operators. This is most notable in Brazil, where independents account for 91% of foodservice value sales, compared to 64% for Chile. The higher penetration of chained operators has been key to Chile’s recovery, as restaurant chains tend to have the economic backbone to withstand and resolve unforeseen macroeconomic events, and therefore help restart the industry.

Limited-service restaurants turn price sensitivity into an opportunity

In line with being the country with the most shopping centres in the region, Chile has the highest share held by limited-service restaurants in Latin America (54% of total foodservice value) followed by Argentina (38%). This is an important consideration, given the appeal of limited-service restaurants to many price-sensitive consumers. A high share for limited-service restaurants also positions Chile as the country with the highest transactions per outlet, compared to Mexico, which ranks lowest.

However, Chile also has the highest average foodservice price in Latin America, averaging USD9 per transaction, followed by Colombia (USD6). A reason average spend is rising is that limited-service restaurant operators have managed to premiumise the category, offering products with similar characteristics to higher end restaurants, using gourmet ingredients and food that suggests home-made quality, successfully distancing themselves from connotations of junk food. Consumers are willing to pay more for this, if maintained at affordable prices.

Price strategy to determine how fast markets recover

Most countries in Latin America are expected see recovery in value terms by 2026. But there are factors that could stall growth. Inflation will play a pivotal role, and can be expected to push consumers to opt for cheaper options or reduce their purchase frequency. Higher prices for supplies, logistics and increased difficulties sourcing some imported ingredients will place operators under pressure to externalise costs, and the final price paid by consumers to rise further.

Although delivery and last mile delivery apps are peaking and reigniting the industry, these could become a problem for restaurant operators in the future, cannibalising sales through the delivery channel and leaving operators with lower margins as a result of paying high fees for the service.

For instance, Peru, one of the most fragmented markets, with a high proportion of independent players, experienced the region’s strongest growth within home delivery, where the share of total foodservice value rose from 3% to 20% in 2021. But considering the high fragmentation of independent operators in the region, to obtain better margins the cost is usually passed on to the consumer, which brings its own challenges.

Restaurant operators need to quickly adapt and strategise. There is strong price competition through promotions within delivery apps, and operators need to focus in adapting their products through added value features, to cater to consumer preferences at an affordable price. While each country has its own very individual market characteristics, Chile sets out a clear example how to achieve this - leveraging price and product quality within limited-service restaurants to navigate the macroeconomic challenges ahead.

Further analysis and key data findings on consumer foodservice in 54 research countries can be found here. These reports provide an in-depth understanding of national market dynamics and essential local insight unavailable elsewhere.