Due to an overall slowdown in e-commerce sales growth, persistently high inflation and an increasingly hostile regulatory environment, the immediate prospects for players in the on-demand delivery space – which appeared so bright during the boom years of 2020 and 2021 – have dimmed slightly in 2022. The prospect of a global recession over the next 18 months could further darken the short-term outlook for the on-demand delivery market.

Expansion of quick commerce slowing following rapid adoption during pandemic

Of all the on-demand delivery models, quick commerce has the most difficult hill to climb. Quick commerce players such as US-based Gopuff expanded rapidly over the last two years, but this expansion was based on sustained double-digit e-commerce growth and easy access to venture capital. Now, as investors and consumers look to tighten their belts – and with regulators increasingly hostile to the dark store model – the quick commerce boom appears to be fizzling out, with players in the space reducing the number of markets they service.

With competition in the quick commerce space escalating just as the short-term outlook for on-demand delivery is worsening, the stage is set for an even more intense round of consolidation in the industry, as larger, better-financed players snap up their smaller rivals or force them out of business. For example, in October, Bloomberg reported that Getir – a Turkey-based quick commerce specialist that can rely on relatively strong financial support – was in talks to acquire Gorillas, a rival quick commerce player headquartered in Germany. While discussions between the two operators are still ongoing, if a deal is ultimately approved, Getir would become the dominant quick commerce company across most of Europe.

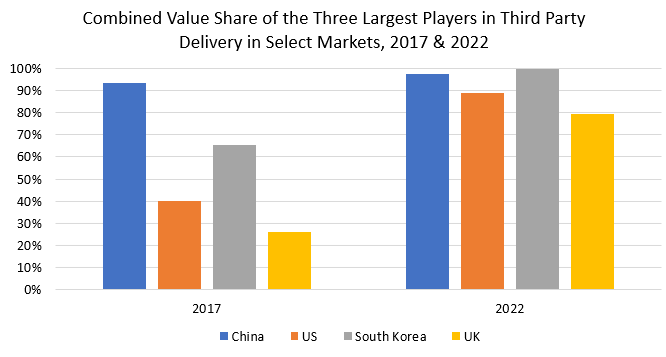

The third party delivery space is also likely to experience an intense round of consolidation. Indeed, the sector has also trended towards greater consolidation over the last few years, as evident by the increasing share of third party delivery sales commanded by the largest players in the industry within the world’s most important e-commerce markets. This development is only expected to intensify as the runaway e-commerce growth of 2020 and 2021 comes to an end.

Note: Value share percentages shown above reflect the share of the three largest players in the combined third party foodservice and third party retail delivery space as of calendar year 2022

Positive outlook for rapid delivery in the longer term

Although the immediate prospects look bleak for many smaller players in the on-demand delivery space, in the long term, the future of rapid delivery appears more upbeat. While it is true that many consumers are eager to return to pre-pandemic shopping behaviour, a substantial portion of store-based sales that migrated to the internet over the course of 2020 and 2021 is unlikely to be recovered. Additionally, many younger consumers are already innately comfortable with shopping online – often on their smartphones – and as their spending power increases, so will on-demand delivery sales.

One reason for optimism regarding the on-demand delivery space is that the world’s leading online retailers seem keen to enter the fray. This trend is especially evident in China. In 2021, JD.com, one of China’s leading online marketplaces, partnered with Dada Group, a Chinese on-demand delivery platform, to launch the Shop Now service, which provides speedy delivery of both grocery and non-grocery retail products. Meanwhile, Alibaba, JD.com’s principal domestic rival, has been an important player in third party delivery since its 2019 acquisition of Ele.me. With the launch of Ele.me’s new chain of bricks-and-mortar Almighty Supermarket outlets in 2022, it now operates what is essentially a quick commerce service as well, as the stores double as fulfilment centres for rapid delivery orders.

Compared to JD.com and Alibaba, Amazon’s on-demand delivery ambitions seem more subdued. Yet it has operated a hyperlocal grocery delivery service in select US metro markets for many years, and in July 2022, it entered into a partnership with Just Eat Takeaway.com that allows the e-commerce behemoth to offer free Grubhub+ membership to its Prime subscription members in the US. (Grubhub+ is the premium membership tier of Grubhub, Just Eat Takeaway.com’s US subsidiary, which allows members to waive delivery fees on all orders.)

Store-based operators look to expand into on-demand delivery, creating further competition

It is not only the digitally native retail leviathans that are attempting to muscle into the on-demand delivery space. Many legacy restaurant operators and retailers that felt forced to partner with third party delivery services during the pandemic are starting to resent paying these services a share of their sales, and many are now looking to build out their own delivery operations, further increasing competition within the industry.

For example, in 2018, Walmart – which remains the largest retailer in the world by sales – sought to address competition from delivery disruptors early by launching Spark, a service that offers same-day delivery by using independent contractors to collect orders from Walmart’s US stores and deliver them to customers. In 2021, Walmart moved to capitalise on the network of gig workers it had built by offering their services to other retailers. This third party delivery service, dubbed GoLocal, now partners with US retailers of all kinds – from small independent grocers to Home Depot, a major chain of home and garden specialist retailers.

The fact that on-demand delivery is now garnering greater attention from the world’s largest e-commerce operators and legacy retailers is undoubtedly a positive sign for the long-term prospects of the industry. Since these companies have the logistics capabilities and the financial support to potentially dominate the sector, it will place greater pressure on smaller players in the space.

Read on about the issues impacting on-demand delivery in our report, Digital Distruptors: The Global Competitive Landscape of Delivery Platforms.