The Impact of HFSS Legislation on Food and Drink in the United Kingdom

The British Government’s anti-obesity regulation on products high in fat, sugar and salt (HFSS) is likely to impact packaged food and soft drinks, both in terms of brands and consumers. Effective from October 2022, the policy prohibits retailers larger than 185 sq m from implementing volume-based promotions on HFSS products, restricts their in-store and online presence, and limits television advertisements. Although the new legislation might come as a hindrance for some categories, it might also offer an opportunity for others.

Impact on sales of food and drinks

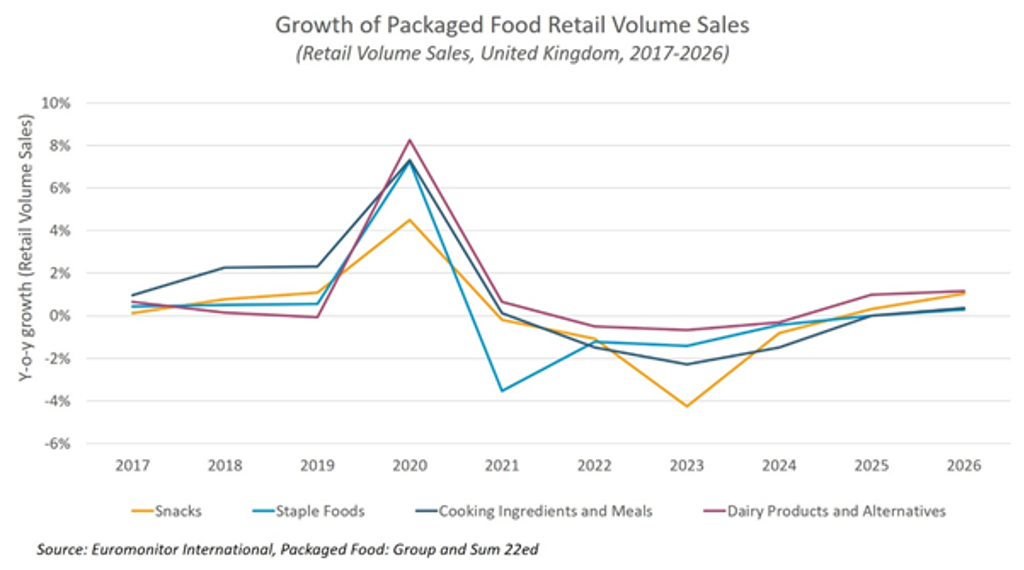

Packaged food sales are projected to lose the momentum gained during the lockdown restrictions in 2020. Given their strong dependence on impulse purchases, cereal bars, chocolate countlines and single-portion ice cream will be among the most impacted snacks categories after losing their prominent in-store positions, while potato chips and puffed snacks are expected to experience further pressure from the ban on volume promotions. Within ready meals, pizza is set to suffer the most, given the limited presence of non-HFSS options, while within staple foods, children’s breakfast cereals and flakes will be particularly challenged by the intensified criticism of their high sugar content.

Opportunities

The HFSS regulation encourages manufacturers to proceed with recipe reformulations or product launches that fall below the HFSS threshold. This will allow them not only to escape the restrictions, but more importantly, to target more health-conscious consumers and expand their offerings to new geographies.

Exempt products have a unique opportunity to consolidate their market presence during the time competitors struggle with restrictions. Among the favoured brands are Eat Real crisps, Kellogg’s Coco Pops and the new Dr Oetker’s The Good Baker pizza, which are already non-HFSS and are expected to gain share by leveraging their health-oriented positioning.

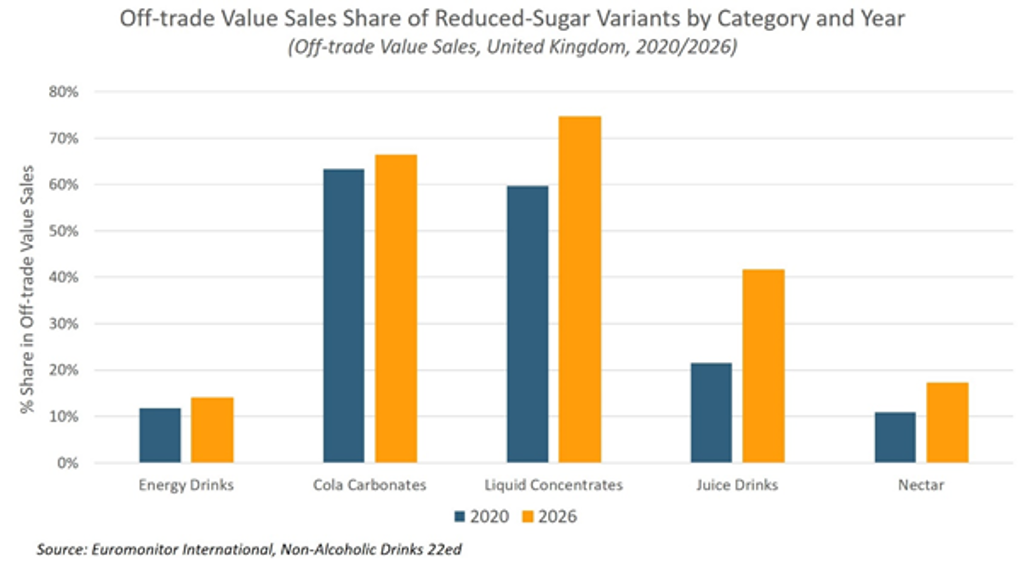

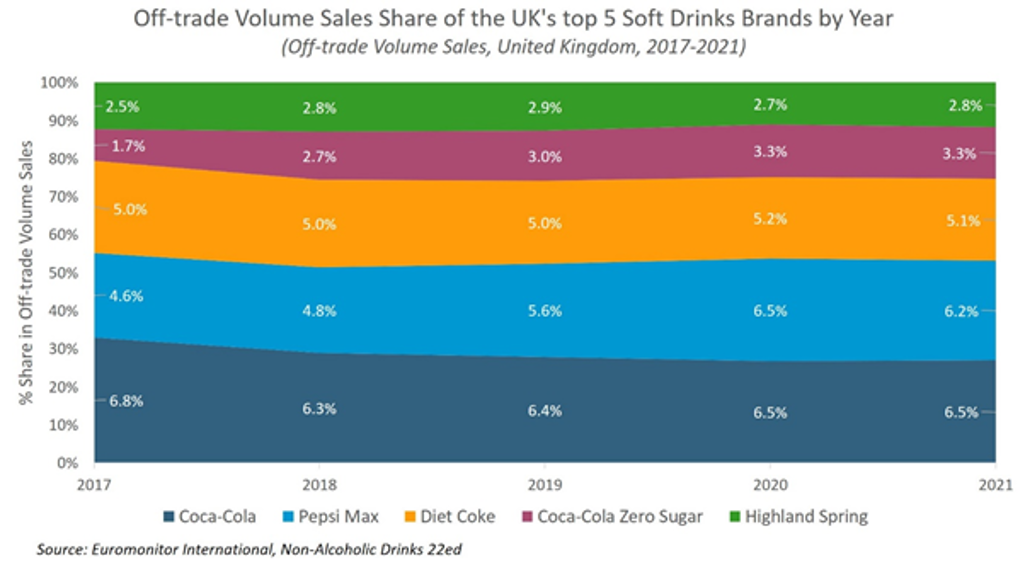

In soft drinks, the popularity of reduced-sugar variants will continue. Currently, three out of the top five brands are low sugar options (Pepsi Max, Diet Coke and Coca-Cola Zero Sugar). In the last five years, the three brands combined have increased their off-trade volume share from 11% to 15%.

Threats

Despite the benefits, reformulation is a complex process as taste is an element that cannot be compromised, especially when it affects children’s satisfaction. As confirmed by 31% of UK parents at Euromonitor International’s Voice of the Consumer: Health and Nutrition Survey 2021, children do not enjoy the taste of healthy food, preventing them from improving their diet.

Promotional restrictions and the increasing cost of recipe improvements are expected to generate price increases. Also reflected in Euromonitor International’s Voice of the Consumer: Health and Nutrition Survey 2021, price is the main factor discouraging diet improvements, according to 38% of UK respondents. Thus, the HFSS regulation will intensify the competition between branded and private label offerings, forcing manufacturers to capitalise on a product’s specific value.

Innovation towards an increasingly regulated industry

When analysing nutritional intake, it is unsurprising that the categories under the regulation’s microscope are by far the main sources of fat, sugar and salt purchases. According to Euromonitor International’s Nutrition System, more than 80% of the daily per capita purchases of saturated fat and salt, and 61% of sugar, come from packaged food, with snacks and staples contributing the most, whereas soft drinks account for 15% of the daily per capita purchases of sugar.

Although it is difficult to predict whether the HFSS regulation will empower consumers to pursue healthier lifestyles, it is already evident that snacks is expected to face the toughest transition period. The regulation reflects the accelerating global trend towards healthy nutrition and similar measures are increasingly implemented by governments around the world aiming to tackle the rise in obesity and diet-related chronic diseases. Consequently, products with a healthier positioning are set to gain in popularity, highlighting that creativity and innovation in packaged food and soft drinks might be more important than ever.