Euromonitor International has identified key factors that will continue to shape food commodity markets, including commodity price volatility, uneven development in food demand, shifts in global supply chains, climate change and sustainability pressures. Keeping abreast of these trends is extremely important for businesses if they are to manage supply risks, adjust sourcing and pricing strategies, identify and seize new market opportunities, and navigate the turbulence of food commodity markets.

As rapid population growth and rising incomes across developing countries in Asia Pacific are driving robust growth in food demand, the region is projected to offer strong potential in terms of agrifood production expansion. On the other hand, in advanced high-income markets, which are largely saturated, vast opportunities are offered by shifting consumer preferences towards healthier, high-quality and environmentally-friendly food products.

While soaring input costs, global supply disruptions and slowing consumer demand are the major risks faced by agrifood companies in the near term, the impact of climate change and environmental pressures are the major long-term challenges to key food commodities.

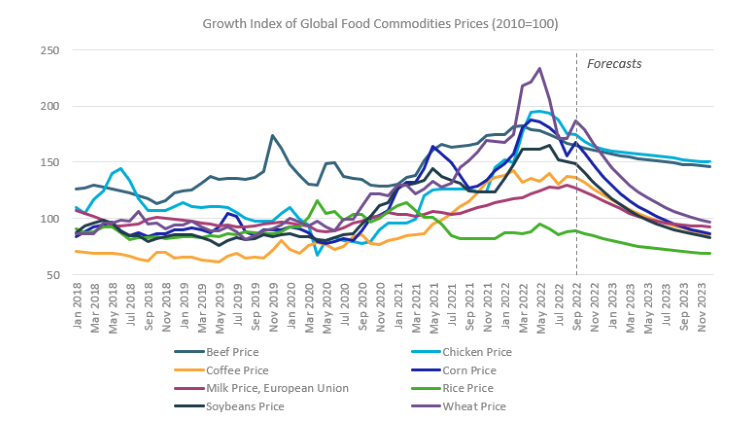

Significant cost pressures and supply disruptions add to food price volatility

Global prices for most agrifood commodities have been rising since 2020, driven initially by surging consumer demand in the wake of COVID-19 and pandemic-related supply disruptions. In 2022, food commodity inflation is being aggravated by weaker output growth due to unfavourable weather conditions, in addition to the ramifications of the war in Ukraine and spiralling input costs (including fertilisers, feed, energy, labour and logistics). Moreover, a wave of agrifood export restrictions in 2022 over domestic food security concerns (including temporary bans on exports of wheat in India, Russia and Kazakhstan, palm oil in Indonesia and poultry in Malaysia), is contributing to the inflation surge.

Inflation for most food commodities is expected to soften over the second half of 2022 and into 2023, due to cooling input costs, improving production prospects and slowing consumer demand. However, these forecasts are subject to a number of risks, such as increased volatility of input costs, tighter-than-expected global supply and the prolonged war in Ukraine.

Uneven shifts in food demand across global markets offer diverse opportunities

While the world’s increasing population will be supporting growth of global food demand, the development of dietary patterns will vary across regions. In developing countries, particularly in Asia, strong population growth, rapid urbanisation and rising consumer affluence are expected to provide a substantial boost to more diverse diets with increasing demand for animal proteins. On the other hand, advanced economies are expected to record modest growth in demand due to relatively high saturation and limited population growth prospects. Changes in food demand across high-income markets will also be shaped by the shift towards plant-based diets, in addition to growing preferences for “free from” foods, including products free from gluten, fat and sugar. Meanwhile, population across the least developed countries will continue to largely rely on staples.

Furthermore, the short- to medium-term outlook for food demand will be highly affected by elevated agrifood commodity prices that are adding to already high food inflation. Faced with an intensifying cost-of-living crisis, cash-strapped consumers may choose to trade down to less expensive food products and staples, or reduce overall food consumption. The lower-income population across import-reliant countries remains most vulnerable to food insecurity.

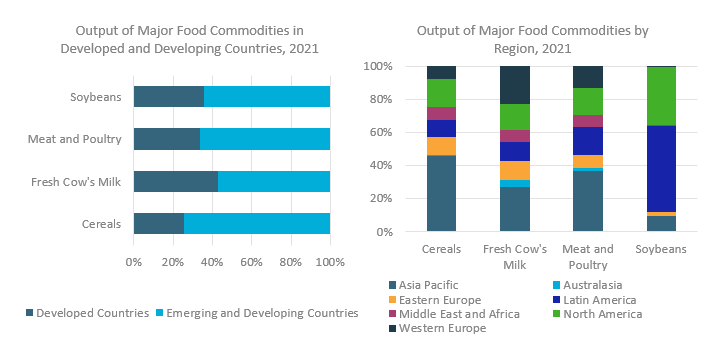

Enhanced production capacity in developing countries in response to rising food demand

Developing economies in Asia Pacific and Latin America are already home to the large share of global agrifood production output, with significant space left for agricultural productivity growth. To meet growing food demand, governments and companies across developing countries are investing in food production intensification, advanced farming techniques and the development of vertical integration of the agrifood industry. As a result, developing economies across Asia Pacific and Latin America, including Brazil, India and Argentina, witnessed some of the largest increases in production output of cereals over 2016-2021, while Indonesia and Pakistan recorded some of the steepest growth rates in meat and poultry output.

Climate change remains a significant risk to food commodity producers

Rising temperatures and extreme weather volatility, along with worsening global water shortages, pose a long-term threat to key food commodities. For example, over 2021-2022, a severe drought hit southern Brazil, north-eastern Argentina and Paraguay amid a continuing La Niña climate pattern. This resulted in shrinking soybean harvests in the 2021/2022 season, pushing up feed prices and undermining the sufficient supply of feed for meat and dairy sectors. Meanwhile, Pakistan, the seventh largest global wheat producer, is facing a climate-related food crisis as heavy rainfall and severe flooding in summer 2022 devastated the country’s farmland.

Regenerative agriculture, smart farming, adaptive crop and livestock management, and crop diversification will be key to withstanding the emerging climate challenges. However, developing nations, which lack resources to address the climate change impact, will remain most susceptible to the negative global warming effects.

Agrifood producers are facing intensifying sustainability pressures

The sustainability of food production is of rising importance, especially in high-income countries, amid growing consumer concerns over food quality, environmental impact and animal welfare. Moreover, increasing social responsibility concerns and emerging fair trade certifications are pushing agrifood companies to ensure fair wages and working conditions for farmers.

To comply with intensifying environmental regulations and maintain competitive advantage, agrifood producers are forced to advance their environmental strategies and embrace sustainable production methods. For example, major Brazilian meat producers JBS, Marfrig and Minerva have pledged to free their supply chain from meat linked to illegal deforestation by 2030.

For further insight, please read Euromonitor International’s global reports on major agrifood commodities, here, and download your copy of our free report, Global Trends in the Commodities Market.