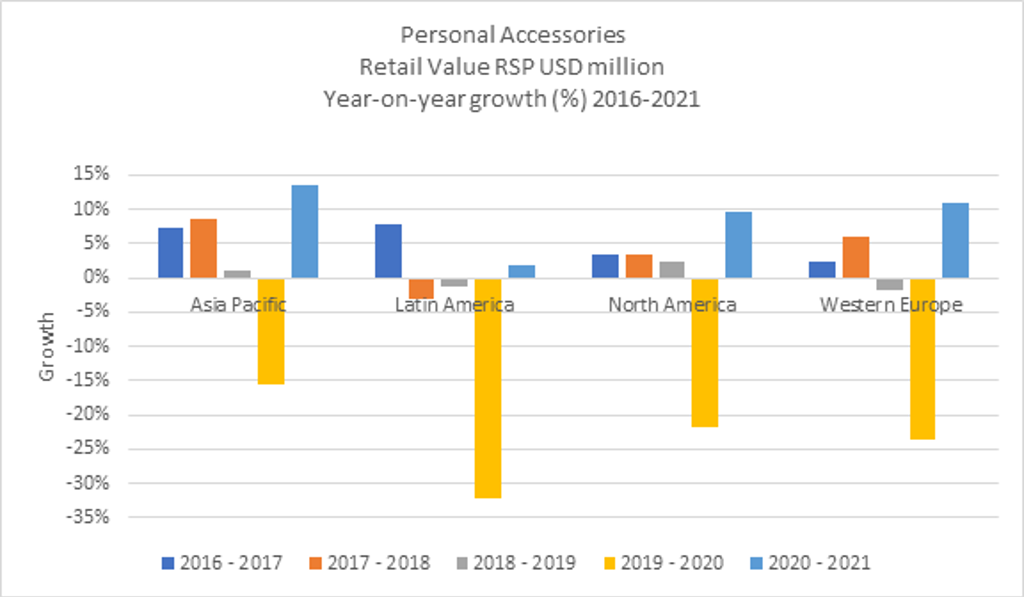

Sales of personal accessories in Asia Pacific declined by 16% in 2020, as the COVID-19 pandemic led to national lockdowns, social distancing, store closures and travel restrictions, thereby causing regional demand to suffer. However, the level of decline was one of the smallest when compared with the 19% global decline, as it was the first region to enter the recovery phase. Furthermore, consumers from Asia Pacific drove sales domestically as they were unable to travel, spend and shop overseas. The industry also benefited from a polarisation in consumer spending, towards either the highest-end brands or the lowest-priced deals, with some consumers buying fine jewellery and other luxury goods as an investment.

The lifestyle changes caused by COVID-19, such as travel disruption, have meant that wealthy consumers in particular have been able to spend more money on discretionary items, including fine jewellery and luxury handbags, as they have been unable to spend in other areas of their lives, such as eating out and travel. Higher domestic spending contributed to an increase in sales of personal accessories in the region, but this only partially compensated for the losses associated with tourism spending.

Factors including attitudinal and consumption shifts, the fast pace of digitalisation and changes in distribution channels have proven crucial in protecting the industry from further sales losses in the region and are anticipated to remain vital in the long-term recovery of personal accessories.

The rapid migration to digital technologies mitigates sales decline

Companies competing in Asia Pacific were forced to enhance digitalisation beyond distribution, as consumers adopted a digital-first mindset pre- and post-purchase. Historically dependent on in-store retailing, players had to invest in e-commerce capabilities and developing complementary in-store digital tools alongside their e-commerce offerings.

Similarly, in Hong Kong, leading industry player Richemont upgraded its online services, providing free home delivery and flexible refund capabilities, whilst also offering the option to order products to try on at home. The company also introduced one-on-one virtual consultations via its brands’ official websites. In China, the adoption of livestream and private domain marketing via WeChat was also seen, with leading luxury players including LVMH and Gucci using livestreaming.

Companies in categories such as eyewear accelerated the deployment of digital services, moving beyond transactional websites towards digital health and remote eye care, to answer the need for accessibility, convenience and immediacy of treatment. They also looked to replicate their in-store offer virtually, including the adoption of augmented/virtual reality tools such as frame try-on at home to maintain engagement and sales. For example, Chinese eyewear retailer Chow Tai Fook rolled out initiatives such as cloud kiosks, a new CRM platform on WeChat, and customised pieces. Meanwhile, Luxottica India Eyewear expanded its digital presence in India through its Smart Shopper digital initiative, which includes the offering of its entire range of products under one single online store and virtual try-on.

Changes in distribution channels in Asia Pacific

Amidst changing consumer preferences in Asia Pacific, as well as the growing middle classes and rising consumer purchasing power in markets such as China and India, the region has accounted for a growing proportion of sales for all companies in recent years. As a result, industry players have prioritised their physical retail and e-commerce footprints in the region. This has become even more crucial during the pandemic, as retailers have sought to grow their brands’ sales in tandem with growing market sizes. Although historically retailers have been dependent on in-store retailing, COVID-19 has forced the industry to rethink its distribution channels to better reach and engage with consumers in Asia Pacific.

In India, retailers experienced a challenging task reaching out to consumers due to the strict lockdown imposed by the government. The lockdown restricted consumers’ movement outside of their homes. To overcome this situation, where consumers were both unable and afraid to go outside, retailers developed innovative approaches, such as setting up mobile retail stores within the premises of housing societies. For example, retailers such as Max Fashion and Reliance Trends worked on setting up these stores within the community area of residential societies over the weekends, which allowed consumers to shop for apparel, bags, sunglasses, etc. from the comfort of their community. Retailers also offered video tours of their stores to consumers to show them their collections. For example, fine jewellery retailer Tanishq offered video tours of its store to consumers. In addition, retailers also visited consumers’ residences to show them their collections at their homes and help them make a purchasing decision. Fine jewellery retailer Tanishq and eyewear retailer Lenskart were amongst the few players that leveraged this strategy.

In the case of Japan, the pandemic resulted in direct-to-consumer brands growing faster than traditional wholesale brands. For example, in the case of fine jewellery and watches, several consumers in Japan still enjoy trying out products before making a purchase. They also prefer styling different pieces of accessories in their daily lives. To cater to this consumer base, subscription services such as Laxus in bags and luggage and KARITOKE in watches are rapidly expanding their user bases following the COVID-19 pandemic. Even spectacles retailer Megane Super has launched a subscription service, where members can replace spectacle lenses or frames for a monthly subscription fee of JPY1,000, JPY2,000 or JPY3,000, depending on the plan. With this, the company is encouraging consumers to have multiple pairs of spectacles for different usage occasions to ease eye stress.

In South Korea, mobile-exclusive brands are gaining traction, as they make it easier to attract consumers, especially the younger generation within the 10-20 age bracket. An example of this is Korean jewellery brand Didier Dubot, which is owned by Sejung Corp. The company worked towards strengthening its positioning by launching Debong Didi, a jewellery line exclusively available at Kakao Gift.

With the pandemic disrupting consumer behaviours, purchasing patterns and income levels, retailers are expected to be creative when focusing on their distribution strategies. In order to stay ahead, companies will have to focus on a stronger omnichannel presence which allows them a competitive advantage. Identifying evolving purchasing trends and channels through which consumers are quite comfortable shopping will transform distribution strategies and help businesses grow globally.