As inflation dominates the global economy, this is the first of a new series of quarterly articles highlighting key insights from Euromonitor’s global inflation tracking report.

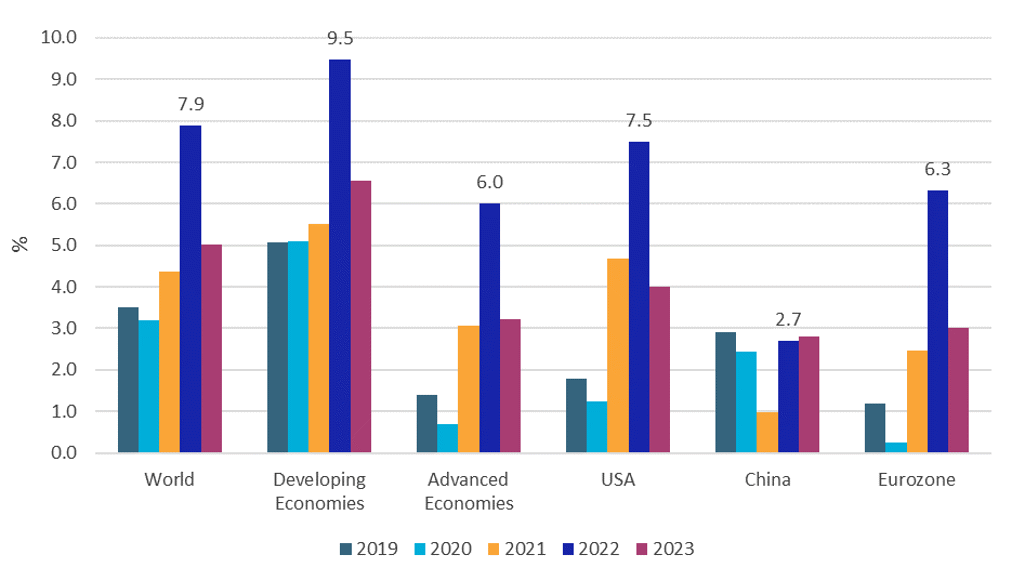

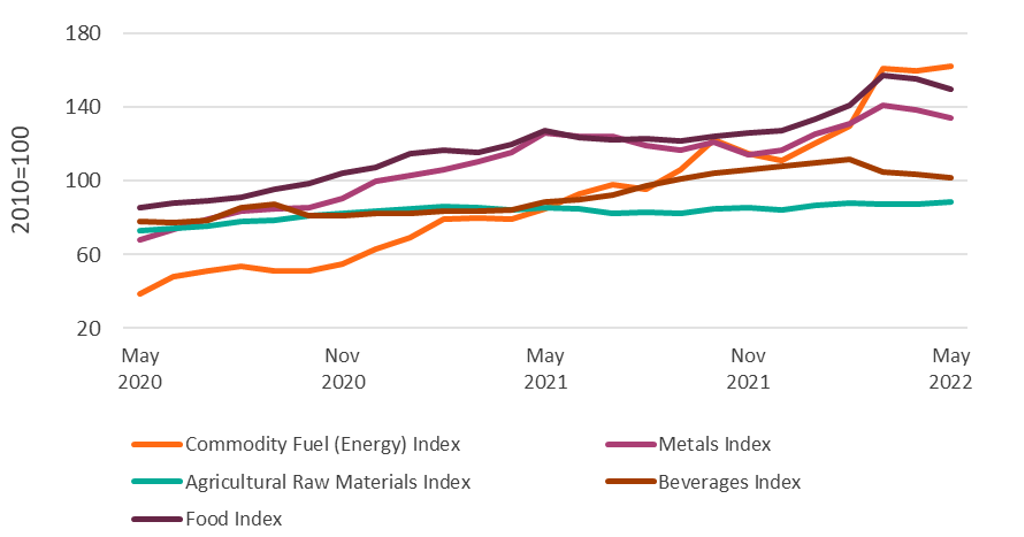

Global inflationary pressures have increased in Q2 2022, following Russia’s invasion of Ukraine. Supply chain and transportation problems, as well as added volatility and rising energy, food and commodity prices, are accelerating global price growth. Although the war will also dampen some inflationary pressures due to lower private sector confidence and spending, overall global inflation is forecast to accelerate in 2022-2023. Under the baseline scenario, global inflation is forecast to reach 7.9% in 2022, and towards 5.0% in 2023, compared with 2001-2019 average annual global inflation of 3.8%.

Overall, countries with greater energy dependency will feel higher inflationary effects in 2022. With inflation forecast to remain at elevated levels in 2022-2023, consumers and businesses in both emerging and developed economies will increasingly feel the squeeze of rising prices. Higher prices will also add more pressure to the profit margins of businesses.

Global Inflation Baseline Forecast, 2019-2023

Source: Euromonitor International Macro Model (updated 11 April 2022)

Note: data from 2022 onwards are forecasts

Rising commodity and energy prices accelerate inflation growth

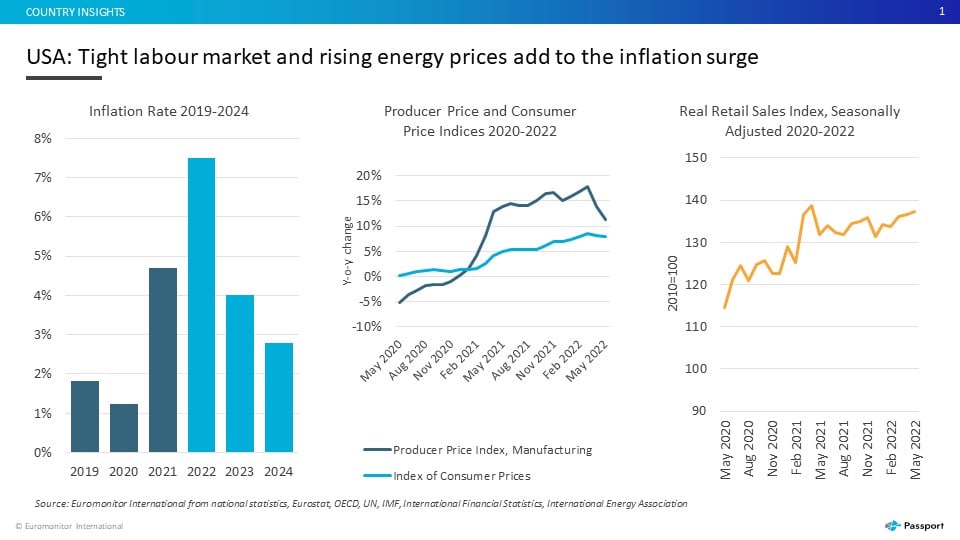

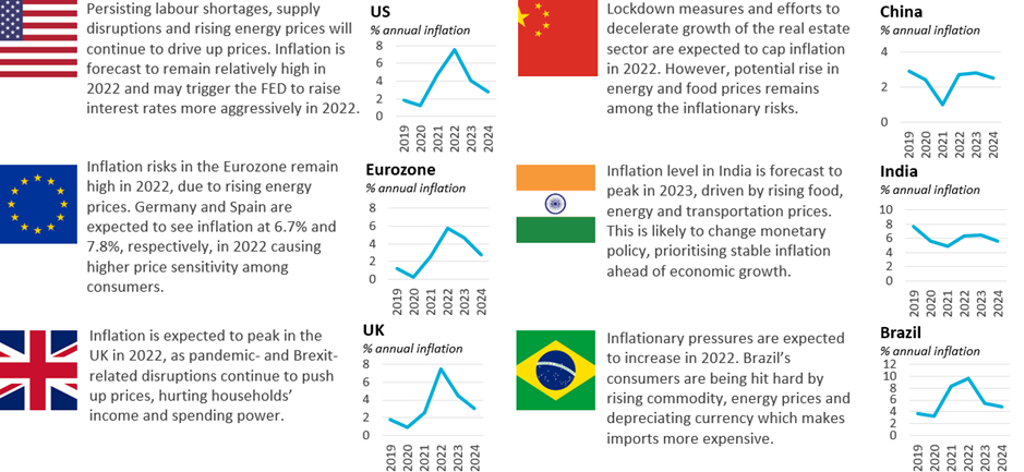

- The inflation rate in the US is forecast to increase to 7.5% in 2022. The level of inflation started to increase after the pandemic, influenced by worker shortages and supply chain disruptions. The Federal Reserve (FED) is taking measures to curb inflation and increase interest rates. However, the tight labour market and surging global commodity prices are making it more difficult to curb inflation to the 2% target.

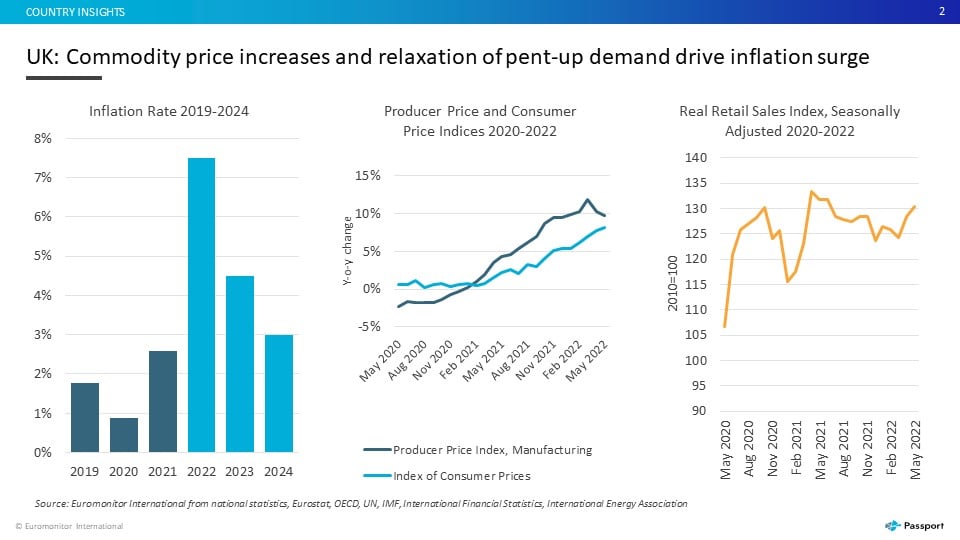

- The inflation rate in the UK is forecast to reach 7.5% in 2022. The increase in inflation is being driven by rising fuel and energy prices, household services and transportation costs. Pent-up demand accumulated during the pandemic and Brexit-caused labour shortages are also contributing to faster price growth. The Bank of England has increased the interest rate to counter inflation, although supply chain disruptions are likely to continue to add to inflationary pressures in 2022.

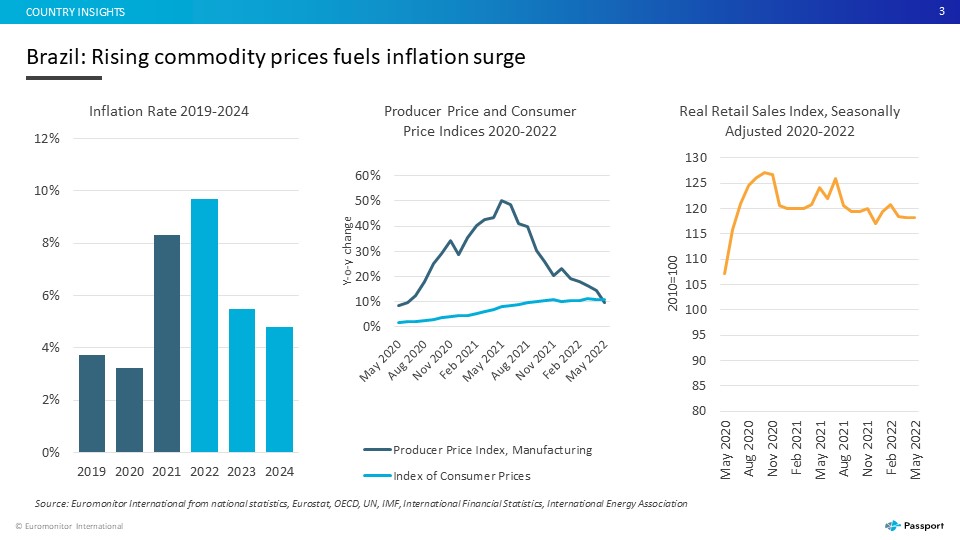

- The inflation rate in Brazil is forecast to reach 9.7% in 2022. Global supply chain disruptions and rising commodity prices are resulting in faster producer and consumer price growth. Furthermore, Brazil’s depreciating currency is also adding inflationary pressures, as imported goods are becoming more expensive. Brazil’s real is forecast to drop 7% in value against the US dollar in 2022 on the back of political uncertainties and low investor confidence.

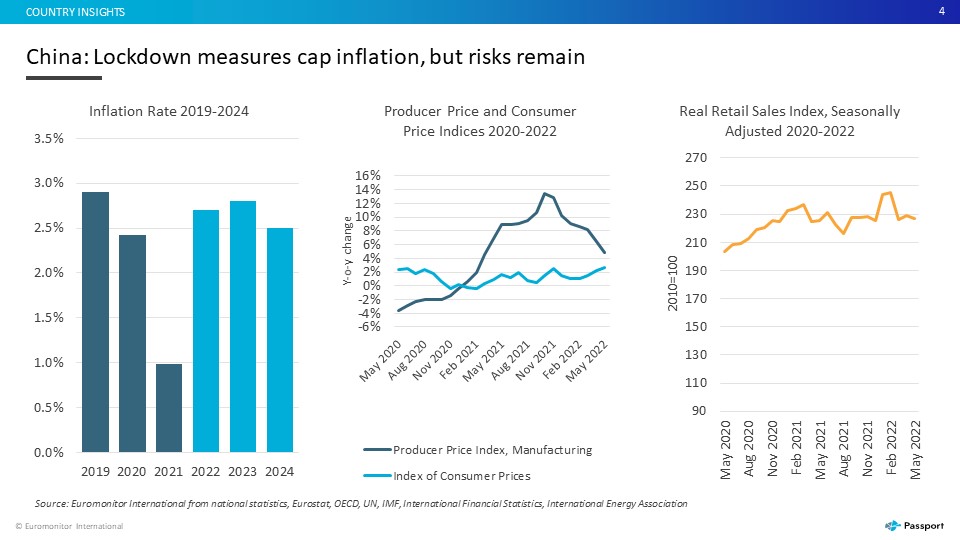

- The inflation rate in China is forecast to reach 2.7% in 2022. China’s zero-COVID policy and efforts to decelerate the growth of the real estate sector are resulting in slower economic growth, and in turn a lower inflation rate. However, China remains vulnerable to potential price increases due to rising energy and agricultural commodity prices. As of 2021, China imported 49% of crude oil and gas.

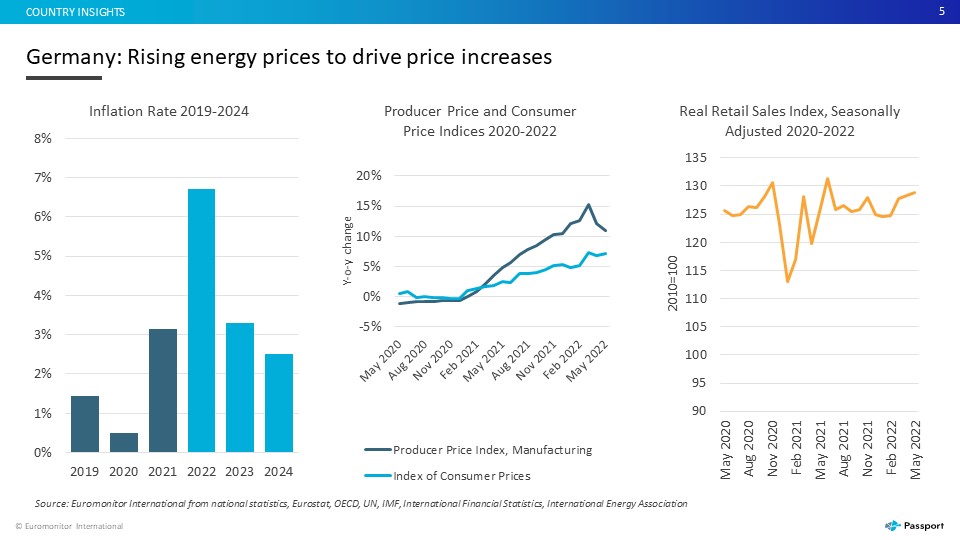

- Inflation risks in the Eurozone remain high in 2022, largely the result of rising energy prices. Countries with high energy dependence, such as Germany, Italy and Spain, are expected to see sharper price increases, with inflation forecast at 6.7%, 6.5% and 7.8%, respectively, in 2022. Consumers and businesses in the Eurozone will increasingly feel the squeeze of rising prices during 2022-2023. Higher prices will also add more pressure to the profit margins of businesses.

Key Country Insights

Source: Euromonitor International from national statistics, Eurostat, OECD, UN, IMF

Downside risks remain significant

Russia’s invasion of Ukraine is the main risk contributing to higher inflationary pressures. Higher volatility in commodity markets, supply disruptions and transportation problems are forecast to disrupt global supply chains and inflate input prices. Restrictions on Russia’s crude oil imports in Europe, as well as efforts to reduce reliance on natural gas, will also result in energy price shocks and impact global B2B, transportation and logistics sectors.

Ongoing labour market problems in the largest economies are expected to inflate operating costs for companies and add to the rising level of inflation. Shortages of workers are predicted to drive wage increases and pressure companies. China’s zero-COVID policy could also contribute to global supply problems.

Lastly, extreme weather conditions is predicted to be a long-term trend that could contribute to growing inflation, threaten agricultural yields and food security, and may trigger trade protectionism. The current dry and hot weather in France and India, and droughts in the US and Canada have raised concerns about lower crop yields in these major grain producers in 2022.

Global Commodity Price Indices, 2020-2022

Source: Euromonitor International from national statistics, World Bank

To learn more about inflation trends, access the Global Inflation Tracker: Q2 2022 report.