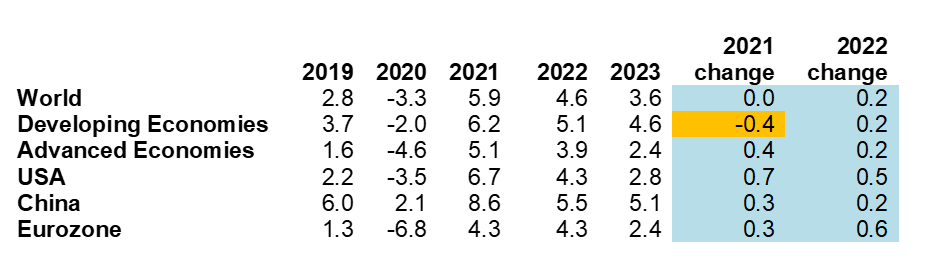

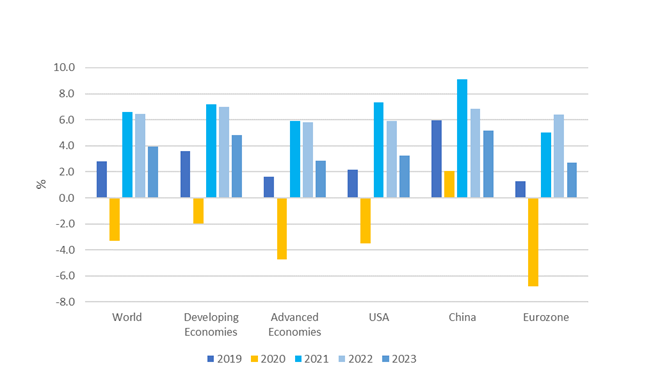

The global economy is now experiencing a fast recovery with growth likely to approach 6% in 2021 (with a plausible range of 5.5-6.5%) and continue at 4.6% in 2022 (with a plausible range of 3.8-5.3%). The 2021 global real GDP growth forecast has remained unchanged relative to Q2, but this reflects a 0.4 percentage points upgrade for advanced economies, offset by a 0.4 percentage points downgrade for developing economies. Global output is estimated to have returned to its pre-pandemic level in mid-2021, but it is expected to remain 2% below the pre-pandemic forecast level even in 2023.

The recovery from the COVID-19 recession has shown strong rebound effects compared to previous global recessions, with moderate longer-term economic activity losses expected. The pandemic may even boost medium to long-term economic growth by accelerating certain productivity-enhancing changes (e.g., the spread of e-commerce, workplace digital technology, e-healthcare).

Real GDP Growth Baseline Forecasts: 2019-2023

Source: Euromonitor International Macro Model, national statistics.

Note: (1) Regional real GDP growth using PPP weights;(2) figures for 2021 onwards are forecasted; forecasts updated 28 June 2021; revisions are relative to April 2021; (3) Blue indicates forecast upgrades; orange indicates forecast downgrades relative to April 2021.

Strong recovery in advanced economies and China, ongoing difficulties in key developing economies

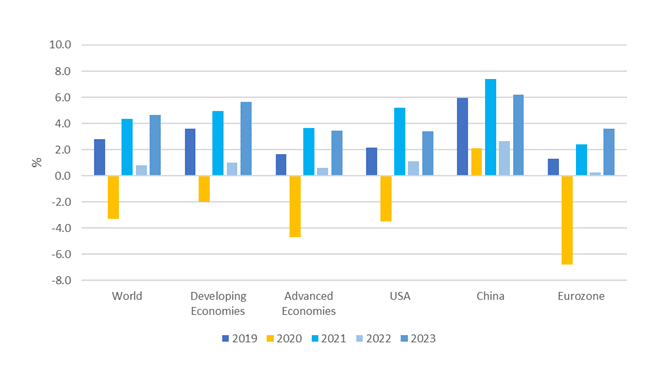

The recovery is stronger in advanced economies, where real GDP growth is expected to exceed 5% in 2021 and approach 4% in 2022 (compared to long-term trend growth of 1.5%). Faster progress on vaccinations has allowed an earlier release of various social distancing restrictions and a large improvement in business confidence. These factors are leading to a fast rebound in consumption and business investment. Advanced economies have also been able to deploy bigger fiscal stimulus packages to aid the recovery, especially in the US where fiscal stimulus is expected to add around 3 percentage points to GDP growth in 2021. After the 4.6% contraction in 2020, the recovery is expected to leave advanced economies’ real GDP level 2.6% below the pre-pandemic forecast level in 2021. By 2023, advanced economies’ real GDP level is expected to slightly exceed the pre-pandemic forecast level in part due to the strong performance of the US economy.

In contrast, progress on vaccinations has been slow in developing economies, with significant coronavirus outbreaks ongoing in Latin America, India, and several other Asian countries such as Indonesia. Developing economies are forecast to expand by 6.2% in 2021 and 5.1% in 2022 (compared to long-term trend growth of 4%). Developing economies’ real GDP level is expected to be 4.4% below its pre-pandemic forecast level in 2021 and 3.7% below the pre-pandemic expectations in 2023. Real GDP in India is projected to remain more than 10% below its pre-pandemic forecast level in 2021, and more than 9% below its pre-pandemic forecast even in 2023. China is an exception to the slower recovery of developing economies, with real GDP in 2021 expected to be just 0.6% below the pre-pandemic forecast level and an almost complete recovery to the pre-pandemic forecast by 2023.

Global economic uncertainty has continued to decline but remains significant

Vaccination rates sufficient for approaching herd immunity are likely to be reached in advanced economies in Q3-Q4 2021, with progress constrained by vaccine hesitancy in certain groups. In developing economies, vaccination campaign progress remains too slow to approach herd immunity before the end of 2022- first half of 2023. The baseline forecast is now assigned a 63-73% probability.

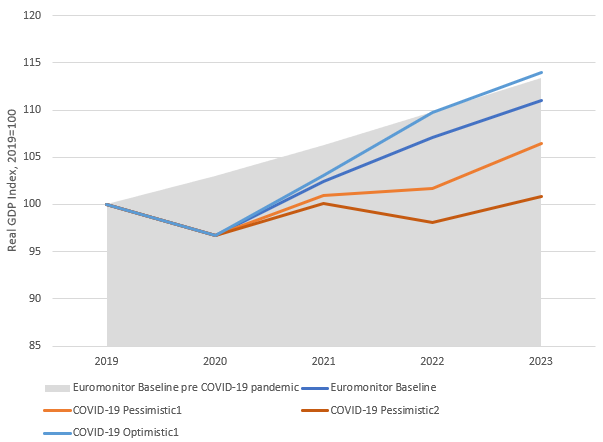

Global Real GDP Index, Baseline and Alternative Scenarios: 2019-2023

Source: Euromonitor International Macro Model, National Statistics.

Note: (1) Global real GDP growth using PPP weights;(2) figures for 2021 onwards are forecasted; forecasts updated on 28 June 2021.

The main downside risk factor is the emergence of new more infectious or vaccine-resistant coronavirus variants. The current Delta variant is significantly more infectious than previous variants, requiring a higher vaccination rate to reach herd immunity if it becomes dominant. However existing vaccines remain highly effective against it, and vaccination incentives are likely to increase as the variant spreads. Recent coronavirus waves have also had substantially more moderate economic effects than the initial spring 2020 wave, due to better targeting of restrictions and better private sector adaptation (e.g with more substitution towards online services and retailing, more durable goods purchases for the home). Therefore, in the baseline forecast the economic effects of the Delta coronavirus variant are mild in advanced economies, disrupting the recovery more significantly in key developing economies such as India.

However, uncertainty about the effects of new virus variants remains significant. In the COVID-19 Pessimistic1 scenario, the spread of more infectious and vaccine-resistant COVID-19 mutations would cause a renewal of more intense lockdowns and social distancing measures than at the end of 2020-early 2021. In this scenario, vaccination rates sufficient for herd immunity would be delayed in advanced economies into Q4 2021- Q3 2022. Vaccination rates in developing economies would remain too low for approaching herd immunity into 2023. Longer lasting and more severe social distancing restrictions would reduce global real GDP growth to 4.4% in 2021 and to 0.8% in 2022. This scenario is still assigned an 18-28% probability in Q3 2021.

Real GDP Growth COVID-19 Pessimistic1 Scenario: 2019-2023

Source: Euromonitor International Macro Model, National Statistics.

Note: (1) Global real GDP growth using PPP weights;(2) figures for 2021 onwards are forecasted; forecasts updated on 28 June 2021.

Upside growth factors include faster and more substantial consumer spending out of the high cumulated savings stocks of advanced economies’ households, stronger fiscal stimulus effects and a further speed-up in vaccination campaigns. In the COVID-19 Optimistic1 scenario these factors would boost global real GDP growth to 6.6% in 2021 and 6.4% in 2022. This scenario is now assigned a 3-8% probability.

Real GDP Growth COVID-19 Optimistic1 Scenario: 2019-2023

Source: Euromonitor International Macro Model, National Statistics.

Note: (1) Global real GDP growth using PPP weights;(2) figures for 2021 onwards are forecasted; forecasts updated on 28 June 2021.

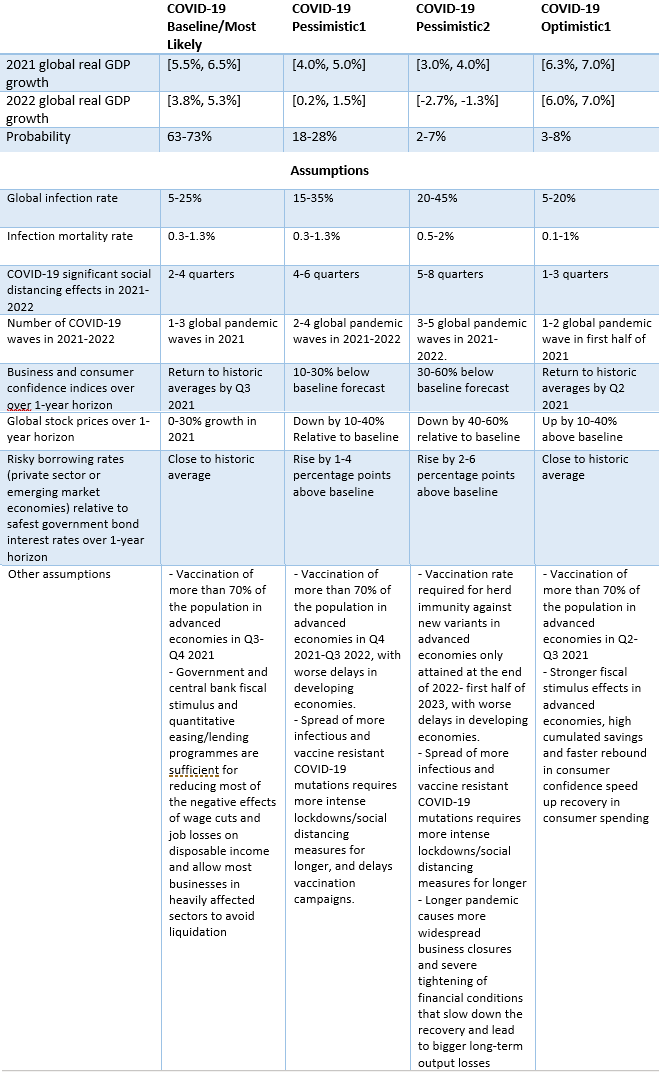

COVID-19 Global Scenario Probabilities and Assumptions: July 2021