Beauty and personal care is a lucrative industry for cannabis-derived products, which Euromonitor estimates to be USD12 billion globally in 2018. North America is at the centre of cannabis beauty and personal care, given the legalisation of recreational marijuana in Canada and 11 US states and a congressional committee approval of a November 2019 bill that would legalise marijuana on a federal level, if passed by the House and the Senate.

Steady growth in the North American beauty and personal care market (3.8% in 2019), a much-touted link between cannabis and wellness and the changing regulatory landscape contribute to the rapid pace of cannabis beauty and personal care growth. As a result, a plethora of beauty brands have entered the market within a relatively short period of time in order to meet aggressive consumer demand, but to also get ahead in a highly fragmented market.

As players look to better understand the market, data that provides a snapshot in time can help provide a foundation in order to track trends and more concretely assess where opportunities lie.

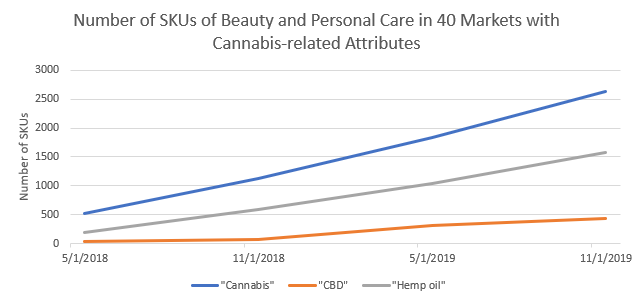

The number of products with cannabis-related attributes is rapidly growing since 2017

Source: Euromonitor International

The number of beauty and personal care SKUs featuring cannabis-related attributes (e.g. CBD or hemp oil) increased 161% over a one-year period up to November 18, 2019 across 40 markets. The increase was greatest among SKUs that were marketed as containing CBD, a 568% increase, while cannabis increased 135% over the same time period. The explosion of growth in the usage of CBD compared to other terms like cannabis and hemp oil confirms a change in marketing. Brands that have had hemp in their marketing for many years (e.g. Hempz and The Body Shop) are now marketing with CBD.

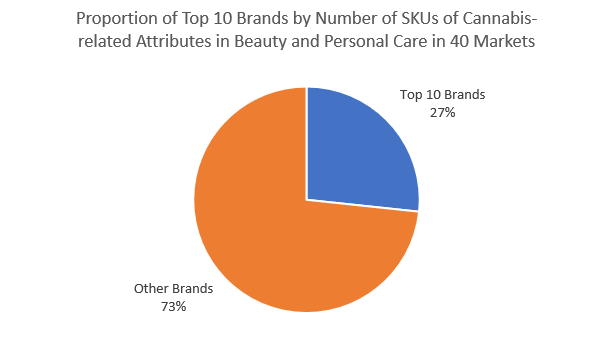

Fragmentation of brands makes it challenging for players to gain significant market share

The proliferation of brands and SKUs containing cannabis-related attributes is contributing to a highly fragmented market. As of November 18, 2019, there were more than 500 brands featuring approximately 4,300 SKUs of cannabis-related attributes across 40 markets. The top-10 beauty and personal care brands with cannabis-related attributes made up only 27% of SKUs.

Source: Euromonitor International

Despite the fast growth of cannabis-related attributes in beauty and personal care, the share of brands is nominal compared to the number of brands in overall beauty and personal care. As of a November 18, 2019, cannabis beauty and personal care brands made up 4.1% of all beauty and personal care products, compared to 2.2% share one year prior, confirming that the market is small, but growing fast within a short period of time.

The cannabis terminology used in brand marketing adds to consumer confusion

Although there is a difference in the functionality and benefits of hemp oil and hemp seed oil versus CBD, hemp oil and hemp seed oil have piggy-backed on the popularity of CBD and are considered by the beauty industry as a cannabis-related attribute, as seen in a 164% increase in beauty and personal care products with hemp oil over a one-year period up to November 18, 2019. However, the growth of hemp oil as an ingredient attribute relies on how manufacturers choose to label ingredients when referring to hemp.

Cannabis sativa seed oil is another name for hemp seed oil. However, some brands are choosing the term cannabis sativa seed oil, rather than hemp seed oil, to capitalise on the association. The implication is that consumers may mistakenly expect certain benefits from a product that are not founded, which may contribute to greater consumer confusion about the efficacy or function of cannabis-related beauty and personal care products.

Looking forward

The US will continue to be the leading market of interest, given the penetration of cannabis beauty and personal care products relative to other markets. The various terminology (cannabis, CBD, hemp oil, cannabis sativa seed oil, etc.) will likely contribute to consumer confusion, in the absence of regulatory guidance that defines each ingredient. Much attention should be paid to the regulatory landscape, which can either hinder or promote the already fast-paced environment of cannabis-derived products. Despite the fast pace and fragmentation of the industry which make it difficult for players to measure market leaders and areas of opportunity, Euromonitor data can be utilized to give visibility to blind spots and identify white spaces of opportunity.

What attributes does Euromonitor consider when analyzing cannabis?

Cannabis is an umbrella term that refers to two species of the cannabis plant, hemp and marijuana. Both hemp and marijuana contain over 100 cannabinoids, of which CBD is currently the most widely popularized. CBD can be derived from either hemp or marijuana. Another related ingredient is hemp seed oil, also referred to as hemp oil or cannabis sativa oil, which is extracted from the seeds of hemp and does not contain CBD. Because of the various terms used to refer to cannabis driven by a lack of standardization, Euromonitor’s classification of cannabis-related attributes used in this analysis includes cannabis, CBD and hemp oil.

This analysis was done using Via, Euromonitor International’s latest pricing intelligence tool. To understand the impact of e-commerce data in the pricing strategy process, download our white paper “How to Optimise Your Pricing Strategy Using Ecommerce Data.”